Understanding Medicaid's Safety Net for Senior Healthcare

Let’s start with Margaret, a 72-year-old widow. Her Medicare plan is a big help, but it doesn't cover the full cost of her prescriptions or the in-home aide she relies on. Margaret’s situation is common. Many seniors find that Medicare, while essential, wasn't built to handle every health expense, leaving serious gaps for long-term needs. This is precisely where Medicaid provides a critical safety net.

Here’s a helpful way to look at it: Medicare is like the strong roof over your head, shielding you from big events like a hospital stay. But a house needs more than a roof to be a home. Medicaid acts as the foundation and walls, offering the day-to-day support that makes life manageable. It’s designed to cover the long-term care that is so important for a person's well-being but often isn't part of a standard Medicare plan.

How Medicaid Creates a Complete Healthcare Picture

Medicaid's main purpose for seniors is to bridge these gaps and make healthcare financially possible. This isn't a small program; its support is vital for millions. In fact, over 7 million seniors aged 65 and up rely on Medicaid for care they couldn't get otherwise. You can discover how Medicaid supports older adults to see the full scope of its impact.

This partnership creates a more complete picture of health security for seniors. While Medicare is focused on treating immediate medical issues, Medicaid offers security for ongoing needs by covering services like:

- In-home personal care and nursing home services.

- Help paying for Medicare costs, such as premiums and deductibles.

- Prescription drug coverage that goes beyond Medicare Part D limits.

- Necessary services like rides to and from medical appointments.

Because of this, figuring out what does medicaid cover for seniors is more than just research. It's the first step toward securing a dignified and stable future. When families understand how these programs fit together, they can form a protective shield for both their loved one's health and their finances against sudden and heavy costs.

Essential Medical Services That Transform Senior Care

Medicare is great for handling major medical events, like a hospital stay after a fall. But what about the routine health needs that keep you safe and healthy every day? This is where understanding what does medicaid cover for seniors makes a huge difference.

Think of it this way: Medicare is like roadside assistance for a major breakdown, but Medicaid is the regular maintenance—the oil changes, tire rotations, and fuel—that keeps your car running reliably. It helps make healthcare a practical part of daily life, not just an emergency service.

Going Beyond the Doctor's Office

Medicaid's help isn't just for when you're sick. It covers services that support a senior's independence and quality of life at home. While Medicare might not cover these items, Medicaid often steps in to provide a more complete safety net.

This support turns healthcare from something you only think about when you're ill into a proactive tool for staying well. Key services include:

- Prescription Drugs: For many seniors, Medicaid helps with the high cost of medications. It can even fill the well-known "donut hole" coverage gap in Medicare Part D plans.

- Durable Medical Equipment (DME): This includes essential equipment that makes living at home safer, such as wheelchairs, walkers, hospital beds, and oxygen concentrators.

- Transportation to Appointments: Medicaid often covers non-emergency rides to doctor's offices and clinics, ensuring that getting to an appointment is never a barrier to care.

Filling Critical Gaps in Everyday Health

Some of the most important health services are the ones we use to stay well, but they are often left out of Medicare plans. Medicaid frequently steps in to cover these fundamentals.

For example, many state Medicaid programs offer benefits for routine dental care, including exams, cleanings, and even dentures. The same often applies to vision care, covering eye exams and glasses. These services prevent minor issues from becoming major health problems.

This forward-thinking approach is a key benefit of Medicaid for seniors, as it supports long-term wellness. You can see how these different services work together in this summary of available care options.

To make it clearer, here is a breakdown of how the two programs often handle common medical services for seniors.

Medical Services Comparison: Medicare vs. Medicaid Coverage

This side-by-side comparison shows what Medicare and Medicaid typically cover for common medical services seniors need.

| Medical Service | Medicare Coverage | Medicaid Coverage | Senior Benefit |

|---|---|---|---|

| Routine Dental | Generally not covered | Often covered (varies by state) | Prevents costly dental emergencies |

| Vision & Eyeglasses | Limited to specific conditions (e.g., post-cataract) | Often covered (varies by state) | Improves safety and quality of life |

| Transportation | Only for emergencies (ambulance) | Often covers non-emergency medical transport | Ensures consistent access to care |

| Prescription Drugs | Covered under Part D with gaps and copays | Often covers copays and fills Part D gaps | Makes essential medications affordable |

By covering these essential services, the combination of Medicare and Medicaid allows seniors to focus on maintaining their overall health, giving them greater peace of mind and financial stability.

Long-Term Care Coverage That Changes Everything

This is the point where truly understanding what does medicaid cover for seniors makes a profound difference. Many families are caught off guard when they discover that Medicare, the primary health insurance for seniors, offers very little for long-term, ongoing assistance. Medicaid steps into this gap, providing a real plan for the future that protects both a person's well-being and their financial stability.

Medicaid offers two main paths for long-term care: professional support in a nursing facility or dedicated assistance right in your own home. This choice is vital, as it allows the care plan to fit a senior’s actual needs and personal wishes. Knowing these options is the first step to avoiding the difficult situation of draining your life savings on care that Medicare simply will not cover.

Bringing Care to Your Own Home

For most seniors, the overwhelming preference is to age in place, surrounded by familiar comforts. Medicaid helps make this a reality through Home and Community-Based Services (HCBS) waivers. Think of these state-managed programs as a way to redirect funds that would have paid for a nursing home to instead pay for services that keep a senior safe and independent at home.

The support is customized to the person’s specific needs, which are identified through a formal assessment. This assistance can be quite broad and often includes a combination of personal and practical help. Common HCBS benefits are:

- Personal Care Assistance: Hands-on help with Activities of Daily Living (ADLs) such as bathing, getting dressed, and eating.

- Homemaker Services: Support with everyday tasks like preparing meals, light housekeeping, and shopping for groceries.

- Adult Day Health Programs: A safe place for seniors to receive social engagement and medical supervision during the day.

- Skilled Nursing: Part-time medical care that a licensed nurse provides at home.

When More Support Is Needed: Nursing Home Care

When a senior’s health requires round-the-clock medical supervision, Medicaid covers the costs of institutional care. This is an absolutely essential financial safety net. Without it, the average cost of a nursing home—which often climbs above $90,000 per year—would quickly deplete a family's entire financial history.

For seniors who are eligible, Medicaid steps in as the primary payer for the facility, covering the costs of room, board, and all necessary medical and personal care. This ensures that a senior gets the constant care they need without their spouse facing poverty or their family's inheritance being lost to medical bills.

So, how does Medicaid determine who is eligible? It’s not an arbitrary decision. States conduct a functional needs assessment to see if a senior requires a “nursing home level of care.” This evaluation looks closely at their ability to handle daily activities, making sure the level of support truly matches their condition. For a visual guide to these different paths, you can review our summary of NJ care options. Planning ahead is the best way to stay in control of your healthcare journey.

Medicare Support and Dual Coverage Benefits

Think of your healthcare coverage like having two safety nets. If you happen to fall through the first, a second one is right there to catch you. This is a reality for seniors who qualify for both Medicare and Medicaid, a status known as dual eligibility. For the nearly 9 million older adults in this situation, this isn't just a small advantage—it's a critical financial support system that turns good coverage into great coverage. This partnership allows Medicaid to step in and fill the gaps Medicare leaves behind, creating a much stronger defense against high healthcare costs.

How Medicaid Makes Medicare More Affordable

One of the most significant challenges for seniors on Medicare is managing the out-of-pocket costs. This is where Medicaid steps in as a financial ally. Beyond covering long-term care, Medicaid offers direct financial aid to help with Medicare-related bills through state-operated Medicare Savings Programs (MSPs). These programs can pay for your Medicare Part B premiums, which saves seniors over $170 per month.

On top of premiums, MSPs can also cover Medicare deductibles and coinsurance, which are the costs you'd normally pay after a hospital stay or doctor's visit. There are different types of MSPs, so you may be eligible for assistance even if you don't qualify for full Medicaid. Discover more about how these support programs work on the official Medicaid site. For many, this support makes Medicare almost entirely cost-free.

Beyond Premiums: Comprehensive Coverage Coordination

The financial help doesn't stop with medical bills; it also extends to prescription drugs, which can be a major expense. If you are dually eligible, you often automatically qualify for the Extra Help program, a federal benefit managed by Social Security. This program is designed to help pay for the costs associated with a Medicare Part D prescription drug plan.

This includes helping with monthly premiums, annual deductibles, and the copayments for your medications. This support can transform prescription access from a source of financial anxiety into a predictable and affordable part of your budget.

The real strength of dual eligibility is how well the two programs work together. Consider Medicare your primary insurance that pays first. Medicaid then acts like a dedicated assistant, coming in afterward to pay the remaining balances and make sure no costs are overlooked. This coordinated approach leads to fewer confusing bills and less time spent trying to sort out who is responsible for what. It creates a unified system that supports both your immediate health needs and your long-term financial stability.

Qualifying for Medicaid: Income, Assets, and Smart Planning

Now that you've seen how Medicaid can work with Medicare, the next logical question is, "How do I actually qualify?" The path to eligibility isn't a confusing maze; it's more like a roadmap with clearly marked routes. Learning to read this map is the key to accessing the support we’ve talked about. It's not about finding loopholes but about understanding the rules of the road so you can plan your journey effectively. This knowledge is fundamental to answering what does medicaid cover for seniors, because getting approved is the first step.

Income and Asset Limits: The Financial Roadmap

Medicaid eligibility for seniors primarily looks at two financial signposts: your income and your assets. Think of income as the money coming in each month (like Social Security or a pension), and assets as the things you own (like savings accounts or property). These limits are not the same for everyone; they change quite a bit depending on your state and the specific Medicaid program you need.

A common myth is that you must be penniless to qualify, but this simply isn't the case. Medicaid rules allow you to keep certain things, known as “exempt” assets. There are also important protections for married couples when only one spouse needs care, designed to prevent the healthy spouse from facing financial hardship.

Key exempt assets often include:

- Your primary home (up to a certain value, which varies by state)

- One personal car

- Household furniture and personal items

- A pre-paid burial fund up to a certain limit

These exemptions mean that qualifying for essential care doesn’t require you to lose everything you’ve worked for. You can see how these rules play out in different situations in this breakdown of New Jersey care pathways.

To give you a clearer picture of how these financial rules can vary, the table below shows some typical income and asset limits for different types of senior Medicaid coverage. Keep in mind these are general examples, and your state's specific numbers will be different.

| Coverage Type | Income Limit (Single Applicant) | Asset Limit (Single Applicant) | Special Considerations |

|---|---|---|---|

| Aged, Blind, & Disabled (ABD) Medicaid | Typically ~$943/month (100% of Federal Poverty Level) | ~$2,000 | Covers basic medical care, similar to a regular health insurance plan. |

| Home & Community-Based Services (HCBS) Waiver | Often higher, up to ~$2,829/month (300% of SSI rate) | ~$2,000 | For in-home or assisted living care. May allow income trusts for those over the limit. |

| Nursing Home Medicaid | All income must go to the nursing home, with a small personal needs allowance (~$30-$100/month). | ~$2,000 | Has complex rules for spousal assets and income to prevent impoverishment of the healthy spouse. |

This table shows that the rules change based on the type of care you need. The most important takeaway is to always check your state's specific Medicaid agency for the exact, up-to-date figures.

The Five-Year Look-Back Period: Planning Ahead Is Crucial

To make sure the system is fair, Medicaid has a rule known as the five-year look-back period. When you apply for long-term care, the Medicaid office will review your financial records for the five years right before your application date. They are looking for any assets you gave away or sold for less than they were worth.

For instance, if you gave your child $50,000 as a gift two years before applying for nursing home care, Medicaid would likely impose a penalty. This penalty is a period of time when you are ineligible for benefits, even if your current income and assets are below the limit. The length of the penalty is calculated based on the value of the gift.

This rule highlights why long-term financial planning is so important. It's designed to prevent people from suddenly giving away their savings just to qualify. Making informed decisions well in advance is the responsible way to prepare.

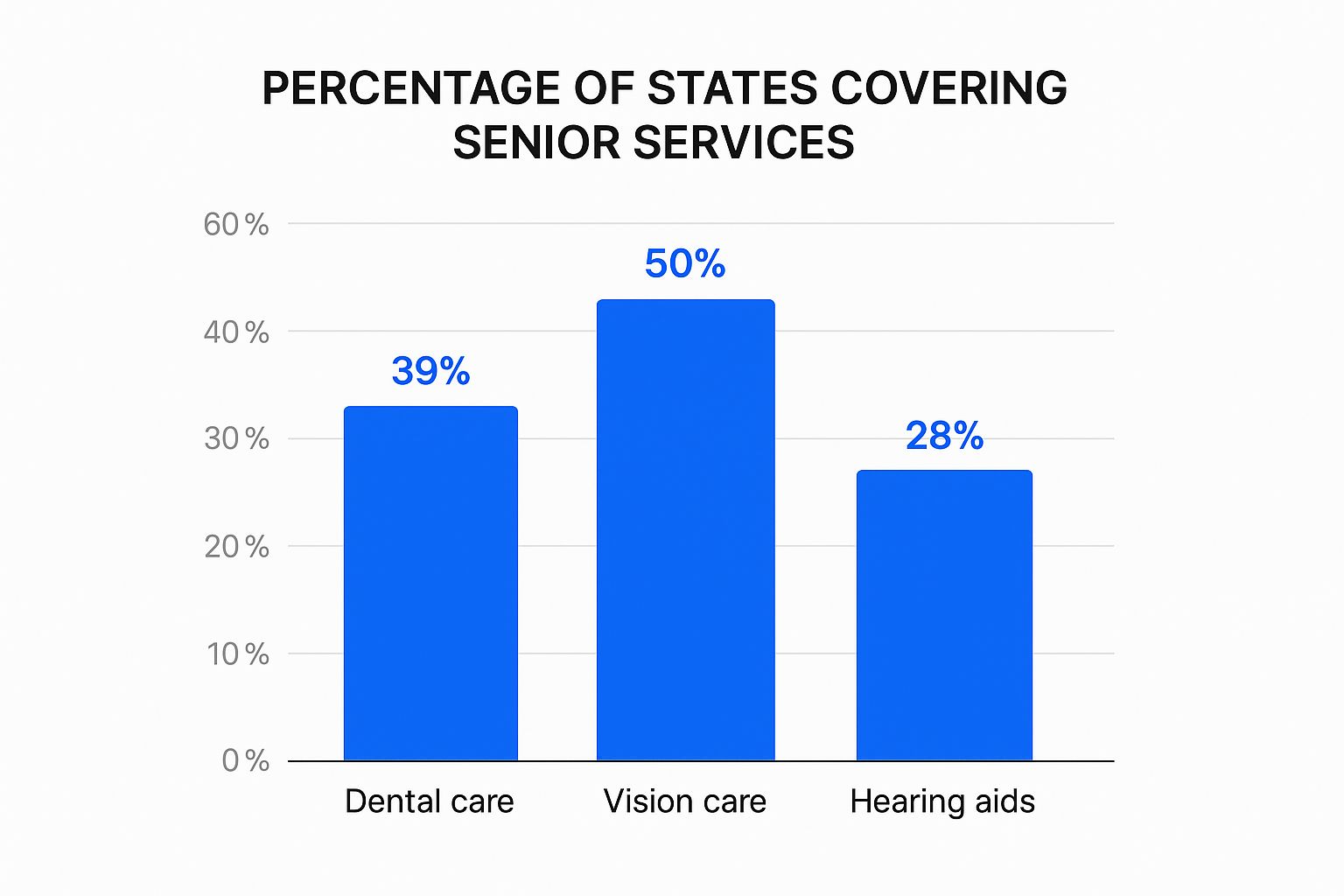

The infographic below shows just how much coverage for other essential services—like dental, vision, and hearing care—can differ from one state to another.

This visual is a powerful reminder that while many states offer at least some dental benefits, far fewer provide comprehensive vision or hearing aid coverage. This makes it absolutely critical to understand the rules not just for Medicaid in general, but for your state's specific programs.

State-by-State Coverage Variations That Matter

While Medicaid is funded by the federal government, each state manages its own program. Think of it like a national restaurant chain where the head office provides the core menu, but each local franchise owner decides on daily specials, operating hours, and hiring practices. This means your home address can drastically change what Medicaid covers for seniors, creating different healthcare realities just by crossing a state line.

A senior living in a state that adopted Medicaid expansion, for example, might qualify for benefits based on their income alone. In a neighboring non-expansion state, the financial rules could be much stricter, making it harder to get approved for the same level of care.

Home Care Access: Waivers and Waiting Lists

One of the biggest differences between states shows up in long-term care, particularly with Home and Community-Based Services (HCBS) waivers. These waivers are optional programs that states can choose to offer, and they are designed to help seniors receive care at home instead of in a nursing facility.

One state might have a strong waiver program that covers everything from personal care aides to adult day care and meal deliveries. Another state’s program might be very limited, or worse, have an enormous waiting list. It’s not unusual for eligible seniors to wait years for a spot to open up. In 2024, over 700,000 Americans were on waiting lists for HCBS, with an average wait time of 40 months. This staggering number shows just how important it is to understand your specific state's policies.

What to Research Before a Move

Moving to be closer to family is a common reason for seniors to relocate, but it’s a decision that requires some homework to avoid losing essential care. Before you start packing, it's critical to look into the rules of your potential new state.

- Income and Asset Limits: Are the financial eligibility rules different from where you live now?

- Specific Services Covered: Does the new state’s Medicaid program cover dental, vision, or the type of in-home help you rely on?

- HCBS Waiver Availability: Does the state have a waiver you can enroll in, or will you be added to a long waiting list?

- Application Process: How long does it usually take for an application to be approved in the new state?

Answering these questions beforehand is the best way to make a smart decision and ensure your healthcare safety net remains strong, no matter where you decide to call home.

Navigating Applications and Getting Approved Successfully

Applying for Medicaid can feel like a huge, complicated task, but it doesn't have to be. Think of it as telling your story to the state—a clear picture of your health situation and financial circumstances. With some preparation and honesty, you can get the support you need to live safely and comfortably.

Your Step-by-Step Application Guide

Following a clear process can remove a lot of the stress and uncertainty. Let’s break it down into a simple, manageable checklist to keep you on track.

Here is a practical guide:

- Get Your Paperwork in Order: Before you even start filling out forms, gather all your essential documents. This includes proof of your age and citizenship, recent income statements, bank records from the last five years, property deeds, and any life insurance policies.

- Fill Out and Submit with Care: Most states let you apply online, by mail, or in person. No matter which method you choose, double-check every detail for accuracy. Small mistakes can cause big delays.

- Be Proactive with Follow-Ups: Don't just submit your application and wait. It's normal for the Medicaid office to ask for more information. A friendly follow-up call can also confirm they’ve received everything and that your application is moving forward.

Tips for a Smoother Approval Process

A few simple strategies can make a real difference in how quickly your application is approved. These tips are based on the real-world experiences of families and social workers who know how to avoid common roadblocks.

- Stay Organized: Keep all your documents in a clearly labeled binder or folder. When you make the caseworker’s job easier, your application can be reviewed faster and more favorably.

- Build a Good Relationship with Your Caseworker: Your caseworker is your primary point of contact, so think of them as a partner in this process. Be polite, respond quickly to requests, and don't hesitate to ask for clarification if something is unclear.

- Know the Timeline: Getting approved for Medicaid isn't an overnight process. It can take anywhere from 30 to 90 days, and sometimes longer depending on your state and the complexity of your case. Setting realistic expectations helps reduce stress.

- Use Free Community Resources: You don't have to figure this out on your own. Your local Area Agency on Aging or SHIP (State Health Insurance Assistance Program) office provides free, expert help with Medicaid applications.

With this information, you can approach the application process with more confidence and a clear plan. For families living in Mercer County, including areas like Princeton and Hamilton, there’s additional local support available. The experienced team at NJ Caregiving provides excellent in-home care and can also guide families through their Medicaid options for home and community-based services. Reach out to us today to see how we can help your loved one maintain their independence and well-being right at home.