What Families Actually Spend On In-Home Care

Let's talk frankly about in-home care costs. It can feel confusing, right? Those hourly rates you see advertised? They rarely tell the full story. Just like buying a house involves way more than just the mortgage payment, in-home care has a range of expenses that can really impact your budget. You might hear about one family paying $3,000 a month, while another pays $6,000 for what sounds like similar services. So, what gives?

This difference often boils down to a mix of things: the level of care needed, where you live, and any extra services required. Basic companionship, for instance, will likely cost less than specialized Alzheimer's care. Plus, the home care industry is booming, fueled by factors like cost-effectiveness compared to other options, and the increasing need for care outside of hospitals. By 2025, the U.S. home care market is expected to hit $225 billion, with the national median cost hovering around $33 per hour for non-medical services. State costs, however, can swing between $24 to $43 per hour. Want to learn more about this growth? Check out this insightful article: GrowthA. This growing market really highlights why transparent pricing information is so vital.

Understanding The Actual Costs

Many families are surprised by hidden costs. These can be things like travel fees, higher rates for weekends and holidays, or minimum hour requirements. Think of it like those unexpected baggage fees on a flight – little costs that add up quickly. Knowing about them upfront helps avoid surprises down the road.

Also, the type of care needed plays a huge role in the final cost. Someone who needs help with a few daily tasks will have a different (and probably less expensive) care plan compared to someone needing 24/7 medical supervision. Understanding the various tiers of service is key here.

For a helpful visual comparison of service levels, take a look at this: NJ Caregiving

Often, families get caught up in hourly rates without really thinking about the total hours needed. This can cause big budgeting problems. It's like comparing grocery prices without considering how much food you actually eat in a week. A lower hourly rate might seem great, but needing more hours at that lower rate can end up costing you more overall. Focusing on the total cost of care is crucial for accurate budgeting.

Let's break down typical costs in a table to make it easier to grasp:

National In-Home Care Cost Comparison by Service Type

Breakdown of average hourly and monthly costs for different levels of in-home care services across the United States

| Service Type | Hourly Rate | Monthly Cost (40 hrs/week) | Annual Cost |

|---|---|---|---|

| Companionship | $25 | $4,000 | $48,000 |

| Personal Care | $30 | $4,800 | $57,600 |

| Home Health Aide | $35 | $5,600 | $67,200 |

| Skilled Nursing | $45 | $7,200 | $86,400 |

Note: These are national averages and can vary based on location and specific needs.

As you can see, the type of care significantly impacts the overall cost. While companionship services offer valuable support, skilled nursing care comes with a higher price tag due to the specialized nature of the services provided. Considering these different tiers of service in relation to your loved one's needs is the first step toward building a realistic budget.

Why Geography Makes Or Breaks Your Care Budget

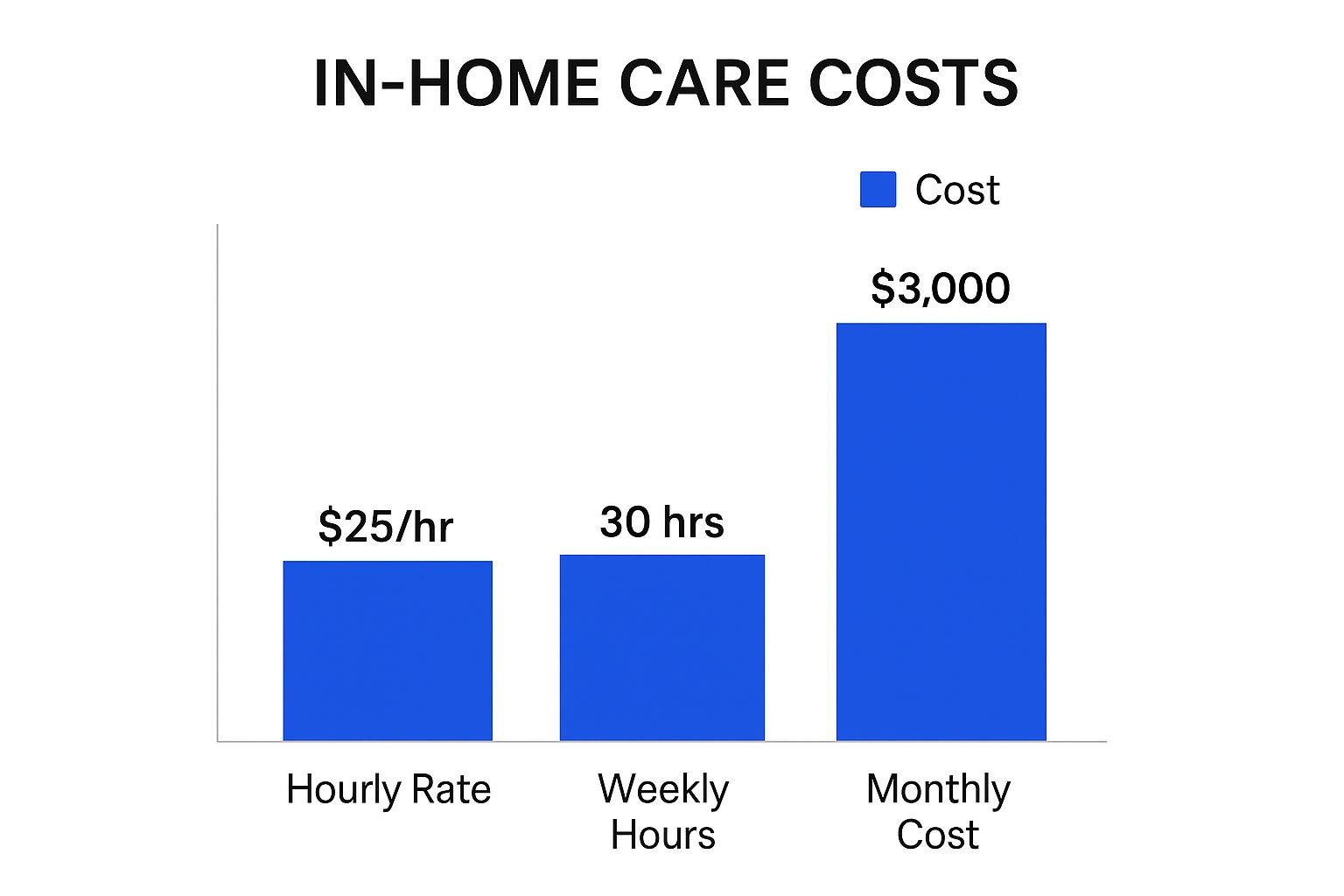

The infographic above shows how your weekly care hours and the hourly rate combine to create your total monthly cost. Notice how even a small difference in the hourly rate can make a big difference in your overall expenses, especially if you need many hours of care each week. This highlights why it’s so important to consider both the hourly rate and the total hours of care when you’re making a budget.

Think about how the price of a cup of coffee can change drastically depending on where you buy it. The same principle applies to in-home care. The cost can vary significantly based on your location. This geographic variation plays a huge role in your overall in-home care cost, so understanding regional differences is crucial for planning ahead financially. The range in cost is wide. For example, 24-hour in-home care can cost anywhere from $15,000 to over $25,000 per month in the United States in 2025. This depends on factors like caregiver qualifications, the types of services needed, and how much demand there is in a particular area. Discover more about 24/7 in-home care costs.

Decoding Regional Differences

Why such a price difference between regions? Several key factors contribute to these fluctuations. One major one is the cost of living. In areas with a high cost of living, like big cities, caregivers need higher wages to afford everyday expenses. This directly impacts what families pay for care.

Another factor is state regulations. States have different rules about caregiver training and certifications. Some states have stricter requirements than others. This can lead to higher costs for agencies to meet those standards, which can then mean higher rates for families.

Market Dynamics and Competition

Think about how real estate works. In a popular neighborhood with few houses for sale, prices tend to be high. The same applies to in-home care. Market dynamics play a big role. Areas with a lot of families seeking care, but not many qualified caregivers, will see higher prices. On the other hand, if there’s less demand and more caregivers available, you’re likely to find more competitive rates. Understanding your local market is a smart way to find good value without compromising on quality.

Exploring Nearby Options

If the cost of care in your immediate area feels overwhelming, consider looking at nearby towns or counties. Sometimes, a short drive can open up more affordable options. This obviously requires thinking about travel time and logistics, but the potential savings can be significant.

For some families, especially those anticipating long-term care needs, relocating to an area with a lower cost of living might be a more drastic, but ultimately more beneficial, option. This is a big decision and needs careful planning, but it can have a huge impact on the overall cost of care.

To give you a clearer picture of these regional variations, let's take a look at the following table:

Regional Cost Variations for In-Home Care Services

Comparison of average in-home care costs across different U.S. regions and major metropolitan areas

| Region/City | Hourly Rate | 24-Hour Care Monthly | Cost of Living Index |

|---|---|---|---|

| (Data needed) | (Data needed) | (Data needed) | (Data needed) |

| (Data needed) | (Data needed) | (Data needed) | (Data needed) |

| (Data needed) | (Data needed) | (Data needed) | (Data needed) |

(Please note that these figures are illustrative and should be replaced with actual data relevant to the intended audience. It’s important to research specific costs in your area.)

This table demonstrates how costs can change from one place to another. You can see the impact of factors like the local cost of living and the market for caregivers in each region. This information can help you better understand what to expect and plan your budget accordingly.

The Hidden Cost Drivers Nobody Talks About

Think of hiring in-home care like going out to a nice restaurant. You see the price of the steak on the menu, but the final bill includes so much more: appetizers, sides, drinks, and that sneaky service charge. In-home care costs work similarly. The hourly rate is just the starting point. Many other factors can significantly impact the overall expense.

Knowing these hidden costs upfront is like checking the wine list before you order – it helps you avoid sticker shock and budget accurately. Ignoring these often-overlooked expenses could double your care costs practically overnight.

Caregiver Qualifications and Experience

Let's say you're hiring a contractor to remodel your bathroom. A seasoned professional with specialized tile-laying skills will charge more than someone just starting. The same principle applies to caregivers. A caregiver with years of experience, specific certifications (like for Alzheimer's or dementia care), or advanced medical training will generally have a higher hourly rate. This isn’t just about seniority; it reflects their specialized knowledge and the quality of care they can deliver. While this might mean a higher cost, it could be a worthwhile investment if your loved one has complex medical needs. The key is to evaluate whether the added expense aligns with their specific requirements.

Scheduling and Flexibility

Just like surge pricing on a ride-sharing app during rush hour, expect to pay a premium for care on weekends, holidays, or overnight. This is standard practice due to the increased demand and the inconvenience for caregivers. Also, keep in mind that many agencies have minimum hour requirements. This means you might have to pay for a set number of hours, even if you only need care for a shorter period.

Personalized Matching and Travel Time

Some agencies go the extra mile by offering personality matching services. They carefully pair caregivers and clients based on shared interests and personality traits, aiming to build a stronger bond and enhance the overall care experience. Think of it like a personalized dating service, but for caregivers. This personalized approach can be incredibly beneficial but often comes with an additional fee. On top of that, travel fees, especially in rural areas where caregivers may have to drive longer distances, can add up surprisingly fast. Keep both these factors in mind when comparing agencies and calculating the total in-home care cost.

Unnecessary Upsells and Negotiation Strategies

Be prepared for potential upsells. Some agencies might try to tack on extra services you don’t really need, much like adding all the bells and whistles at a car dealership. These additions can quickly inflate the cost. Don't hesitate to ask questions, understand the purpose of each service, and negotiate to ensure you're getting the best possible value. Comparing prices and services from different providers is always a smart move.

Real-World Examples and Testimonials

One family, for instance, found that by slightly adjusting their loved one’s care schedule to avoid weekend premiums, they saved $200 each month. Another family negotiated a lower travel fee by agreeing to slightly longer visit times, making it more worthwhile for the caregiver. These seemingly small adjustments can make a big difference in your in-home care cost over time. By understanding these hidden cost drivers and using smart negotiation tactics, you can effectively manage your expenses without sacrificing quality care.

Cracking The Code On Payment Options And Coverage

Figuring out how to pay for in-home care can feel like navigating a maze. It’s a common concern, and understandably so. This section will walk you through the different ways to fund in-home care, explaining options like private insurance, Medicaid waivers, veteran benefits, and long-term care insurance so you can make informed decisions.

Understanding Your Funding Options

I've often heard families ask why some people seem to get a lot of financial help for care, while others in similar situations get little to none. The key often lies in understanding eligibility rules and applying strategically. Timing matters too; some programs have waiting lists or specific enrollment periods.

-

Private Insurance: Think of your private health insurance policy like a menu – it lists what's covered. Some policies offer limited coverage for in-home care, often for services deemed medically necessary. Check your policy details or call your insurance provider to understand what’s included.

-

Medicaid Waivers: These state-run programs offer financial help for in-home care to those who meet specific income and functional needs criteria. Applying can be a bit like filling out a complex puzzle, but these programs can provide vital support.

-

Veteran Benefits: Veterans might qualify for several benefits covering in-home care, including the Aid and Attendance benefit. Eligibility hinges on their service history and how much care they need.

-

Long-Term Care Insurance: These policies are designed specifically for long-term care costs, including in-home care. Think of it like an umbrella for future expenses. The premiums can be substantial, but they offer valuable protection against rising care costs. Most seniors—around 90%—prefer to stay at home rather than move to a facility, according to the National Center for Home Care & Hospice Statistics. This preference is driven by the desire to maintain independence and comfort, along with financial considerations – the average annual cost of home care is about $54,912, often less than many institutional options.

Maximizing Your Coverage

Many families miss out on potential financial assistance because they don’t fully grasp their coverage options or don’t appeal denied claims. Working with a care coordinator or geriatric care manager can be a game-changer. They can act as your guide, helping you navigate the process, pinpoint potential funding sources, and advocate for you.

Combining Funding Sources

Sometimes, the most effective approach is to combine different funding sources. Imagine using private insurance to cover skilled nursing visits, while using veteran benefits to pay for a personal care aide. This strategy can stretch your budget further and ensure more comprehensive care.

State-Specific Programs and Hidden Gems

Beyond the more well-known programs, many states offer lesser-known programs that can offer valuable financial help. Doing your research into these options is essential, as they can significantly lower your out-of-pocket costs.

Planning for the Unexpected

Care needs can change suddenly, like the weather. What works today might not be sufficient next year. Having backup plans is crucial. This might involve exploring alternative funding, tweaking your care plan, or considering different living arrangements.

Practical Tips for Success

-

Documentation is Key: Think of your records as building blocks for your case. Keep detailed records of medical expenses, care needs, and all communication with insurance providers. This documentation is vital for successful applications and appeals.

-

Don't Be Afraid to Appeal: If a claim is denied, don't give up. Many denials are reversed on appeal.

-

Work Collaboratively: Open communication with your care team, insurance providers, and family is key. Working together can simplify the process and lead to better outcomes. By understanding your funding options and planning carefully, you can navigate the complexities of in-home care costs and secure the support you and your family need.

Smart Ways To Cut Costs Without Cutting Corners

Finding affordable in-home care can feel like navigating a maze. You want the best for your loved one, but the costs can be daunting. It's like trying to plan a dream vacation on a shoestring budget – it requires careful planning and resourcefulness. Don't worry, it's possible to provide excellent care without emptying your bank account. Let's explore some practical strategies families use to balance quality care with affordability.

Optimizing Scheduling Patterns

Think about airline tickets: prices skyrocket during peak seasons. Similarly, in-home care often costs more on weekends and holidays. If your loved one's needs are flexible, shifting some care hours to weekdays can lead to significant savings. For instance, if you currently have 20 hours of weekend care at a $35 hourly rate, moving just 5 of those hours to a weekday rate of $30 saves $25 each week. That adds up to over $1,000 in savings annually!

Leveraging Family Resources

Family support is a powerful tool, both emotionally and financially. While professional caregivers offer crucial expertise, family members can contribute in meaningful ways. Think of it as a team effort: everyone pitches in where they can. Perhaps a family member can handle meal preparation, light housekeeping, or simply spend quality time with their loved one. This not only reduces costs but also strengthens family bonds. However, open communication is vital. Be realistic about everyone's capacity to avoid caregiver burnout. You might find this helpful: NJ Caregiving Logo

Package Deals and Negotiation

Many agencies offer bundled service packages, combining services like personal care and light housekeeping at a reduced rate. These deals aren't always advertised, so it pays to ask. Don't hesitate to discuss your budget and needs with the agency. Negotiating rates, especially for long-term care, is often possible. A respectful conversation can lead to an arrangement that works for everyone.

Investing Upfront for Long-Term Savings

Sometimes, a small upfront investment can lead to substantial long-term savings. For example, home modifications like grab bars or a walk-in shower can prevent falls and injuries. While these modifications might seem expensive initially, they can prevent the need for more costly medical care down the line, particularly the high in-home care cost often associated with skilled nursing after an accident.

Avoiding Costly Emergencies

Preventive care is like regular car maintenance – addressing small issues early can prevent major (and expensive) problems down the road. Ensuring medications are managed properly, scheduling regular doctor visits, and maintaining a safe home environment can prevent crises that require costly interventions.

Supplementing Professional Care With Family Involvement

Finding the right balance between professional care and family support is essential for managing in-home care cost. Open communication, clearly defined roles, and realistic expectations are key to making this partnership successful. It's about combining everyone's strengths and availability without overwhelming anyone. This collaborative approach can enhance the quality of care while easing the financial burden.

Building A Sustainable Long-Term Care Budget

Thinking about long-term care finances can feel overwhelming. It's a bit like planning a cross-country road trip – you know the general direction, but there are bound to be detours and unexpected expenses along the way. Building a sustainable long-term care budget is less about predicting the future and more about creating a flexible financial roadmap that can adapt to changing circumstances.

Understanding Predictable Changes

Just like you know gas prices will probably go up during your road trip, some aspects of long-term care costs are relatively predictable. Inflation, for example, will likely increase the cost of everything, including care. The hourly rate for caregivers is likely to rise, just like the price of groceries. Building a buffer for these annual cost increases keeps your budget realistic.

Another predictable shift is the potential increase in care needs over time. Someone who starts with minimal assistance, like help with errands, might eventually need more comprehensive care, such as help with bathing and dressing. This natural progression can significantly impact your in-home care costs. Planning for potential increases in care hours now can prevent financial strain later.

Preparing for the Unpredictable

While we can anticipate some cost increases, others catch us off guard. Think of that unexpected flat tire on your road trip – a sudden expense you didn't budget for. Similarly, unexpected illnesses or injuries can necessitate more intensive, and more expensive, care. A contingency fund acts as your financial spare tire – a safety net for these unforeseen care-related expenses.

Market fluctuations can also throw a wrench in the gears. Changes in the local economy or the availability of caregivers in your area can affect prices. Staying informed about local market trends – like checking gas prices along your route – helps you anticipate potential cost shifts and adjust your budget accordingly.

Practical Budgeting Frameworks

There are several ways to approach your long-term care budget. One way is to project future costs based on current rates and anticipated increases. This is similar to estimating your total trip cost based on current gas prices and mileage. It requires researching local in-home care cost trends and factoring in inflation.

Another strategy is to work backward from your available resources. This involves determining how much you can realistically afford to spend on care – your total trip budget – and then structuring a care plan that fits within those constraints. This might involve combining paid care with support from family or friends.

Expert Insights and Family Case Studies

Just like experienced travelers can offer valuable road trip advice, financial planners specializing in care costs can provide expert guidance. They can help you understand complex financial tools, like long-term care insurance, and create a comprehensive financial strategy.

Learning from the experiences of other families who have navigated this journey can also be incredibly helpful. Case studies offer real-world examples of how families have successfully managed the financial aspects of long-term care, providing valuable insights and potential solutions.

Building Flexibility and Contingency Plans

Flexibility is essential for a sustainable long-term care budget. This means having alternative plans in place, just like having alternate routes mapped out on your road trip. Should your primary funding source change or your loved one's needs increase, you might explore other options like respite care or adult day programs to supplement in-home care.

Contingency planning also involves addressing unexpected events like caregiver turnover. Having a backup plan for finding a replacement caregiver ensures consistent care without disrupting your budget or your peace of mind. By combining careful planning with built-in flexibility, you can create a sustainable long-term care budget that provides security and peace of mind for both you and your loved one.

Your Action Plan For Smart Care Decisions

Now that you understand in-home care costs, let's talk about making smart choices that fit your family's needs and budget. Think of this section as your personalized roadmap for navigating the world of in-home care. We'll cover key cost factors, how to spot potential overpricing, and crucial questions to ask providers.

Creating a Decision-Making Framework

Whether you're planning for the future or need care right now, a solid plan is essential. It’s like planning a road trip: you need a map, a budget, and a plan B in case of unexpected detours. This framework will help you navigate the in-home care process confidently.

-

Define Your Needs: What exactly does your loved one need help with? Is it primarily medical care, or more about assistance with daily tasks like bathing and dressing? Knowing this helps you choose the right type of care and avoid paying for unnecessary services.

-

Set a Realistic Budget: Take a look at your finances and determine what you can comfortably afford. Consider potential long-term costs and explore options like long-term care insurance or Medicaid waivers.

-

Research Local Providers: Compare agencies and independent caregivers in your area. Check out their services, rates, and what their clients have to say. It's similar to hiring a contractor for home renovations – you want someone reputable, reliable, and within your budget.

-

Involve Family Members: Talking about finances can be tricky, but getting the family involved early on prevents disagreements and ensures everyone's on the same page. Open communication is key to making this a team effort.

-

Create a Checklist: Before you interview potential caregivers, make a list of important questions. This could include inquiries about qualifications, background checks, and what happens in case of emergencies.

-

Develop a Contingency Plan: Like having a spare tire in your car, it's wise to anticipate bumps in the road. What if your caregiver is unavailable, or your loved one’s needs change? Having backup plans keeps care consistent, even when things don't go as planned.

Evaluating Providers and Avoiding Red Flags

Choosing an in-home care provider is a big decision. Here are some red flags to watch out for:

-

Vague Contracts: A clear contract outlines services, costs, and cancellation policies. A vague contract is like navigating with a blurry map – it's hard to know where you're going.

-

Pressure Tactics: A reputable provider won't pressure you into making a quick decision. Take your time and choose what's best for your family.

-

Lack of Transparency About Fees: Be cautious of providers who avoid discussing costs upfront. All fees should be clear and easy to understand.

-

Poor Communication: Responsive and clear communication is crucial for a smooth caregiving experience.

-

Negative Reviews or Testimonials: Online reviews and personal recommendations can offer valuable insights into a provider’s reputation.

Ongoing Cost Management

Managing in-home care costs is an ongoing process. Regularly review your budget, look for ways to optimize care schedules, and talk openly with your provider about any financial concerns. Think of it like car maintenance – regular check-ups and adjustments keep things running smoothly.

Making Decisions with Confidence

By following these guidelines and planning thoughtfully, you can navigate in-home care decisions with confidence, knowing you’re making the best choices for your loved one and your family.

Ready to explore personalized in-home care options? Contact NJ Caregiving today at https://njcaregiving.com for a free consultation. We serve Mercer County, including Hamilton, Princeton, and surrounding areas, and are committed to providing compassionate, tailored care that enhances quality of life.