When you start thinking about long-term care, it's easy to get overwhelmed. But putting off the financial conversation is one of the biggest risks a family can take. The reality is that professional nursing home care is incredibly expensive, and without a plan, it can wipe out a lifetime of savings in a shockingly short amount of time.

This isn't about scaring you—it's about empowering you. Knowing the real numbers is the first step to taking control and protecting what you've worked so hard to build.

The Reality of Long-Term Care Costs

The goal of planning is to legally and ethically reposition your savings and property. You want to ensure they aren't considered "countable assets" when it comes time to determine Medicaid eligibility for long-term care. This involves smart legal tools, like Irrevocable Trusts, and a deep understanding of complex rules, like Medicaid's five-year look-back period.

The Staggering Price of Care

The soaring price tag on nursing home care can drain even a healthy estate faster than most people imagine. Depending on where you live, you could be looking at costs ranging from $8,000 to $13,000 per month. These numbers underscore just how critical it is to start planning long before a health crisis ever hits.

For the vast majority of families, those figures are completely unsustainable. This immense financial pressure is why Medicaid has become the country's primary payer for long-term care. The catch? Qualifying for Medicaid isn't a simple process; it means navigating a maze of intricate financial regulations.

The key takeaway is that waiting until you're in the middle of a health emergency will drastically limit your options. Being proactive opens up a whole world of strategies to protect your family's financial future.

Why You Need a Proactive Strategy

Hoping for the best simply isn't a strategy. The government has very specific rules in place, like the five-year look-back period, designed to prevent people from just giving away their assets at the last minute to qualify for help. A well-crafted plan ensures you can meet these requirements legally while preserving your legacy for your loved ones.

So, what does a solid strategy look like? It really boils down to a few key things:

- Early Planning: The most powerful asset protection tools require you to act years before you might need care.

- Legal Instruments: This means using the right legal structures, like trusts, to shield your assets properly.

- Professional Guidance: You absolutely need to work with an experienced elder law attorney who lives and breathes your state's specific rules.

This kind of preparation is the only reliable way to secure quality care down the road without forcing your family to sacrifice their financial security. For a more detailed look at this, our guide on long-term care planning is a great resource.

Getting to Grips With Medicaid’s Rules

To have any chance of protecting your assets from nursing home costs, you first have to understand the system you’re up against. Medicaid is the single largest payer for long-term care in the country, but it’s not a free-for-all. It's a needs-based program with very strict financial rules designed to gatekeep who gets benefits.

Think of it as a complex game. You can’t develop a winning strategy until you know the rulebook inside and out. These rules are designed to ensure only people with genuinely limited resources get help, which means they take a hard look at your income and, more critically, your assets. For families new to this, the requirements can feel impossibly strict, but they're the bedrock of every asset protection plan.

The Five-Year Look-Back Period

The first rule everyone needs to burn into their memory is the five-year look-back period. This is Medicaid's primary defense against people giving away all their money to their kids right before applying for benefits. When you submit that application, Medicaid officials will put every single one of your financial transactions from the last 60 months under a microscope.

Any money or property you transferred for less than it was worth—like signing the house over to your son or giving large cash gifts—triggers a penalty. It’s not a fine you pay; it's a period of ineligibility where Medicaid won't cover the nursing home bill. This penalty is calculated based on the value of the assets you gave away, potentially leaving your family on the hook for months or even years of care costs they can't afford.

For those in Texas, this guide on how to protect assets from Medicaid offers some valuable state-specific insights into this process.

Understanding Asset and Income Limits

Medicaid eligibility boils down to one thing: your "countable assets" must be below a specific, very low threshold. While the exact number varies a bit state by state, the asset limit for a single person needing nursing home care is typically just $2,000. Yes, you read that right. It’s this shockingly low number that forces so many hardworking people to burn through their entire life savings before they can qualify for help.

So, what gets counted? Pretty much everything you’d expect:

- Checking and savings accounts

- Stocks, bonds, and mutual funds

- Any real estate that isn't your primary home

- A second car

The good news is that not everything counts against you. Medicaid does allow you to keep certain exempt assets, like your primary home (up to a certain equity limit), one vehicle, a pre-paid funeral plan, and your personal belongings. The process of strategically rearranging and spending down your money to hit these limits is a key part of qualifying. We offer a deeper dive into this with our guide on the Medicaid spend-down rules.

To make sense of these strict limits, it helps to see the numbers in one place.

Key Medicaid Eligibility Numbers at a Glance (2025 Examples)

This table breaks down some of the most critical financial thresholds for Medicaid nursing home eligibility. It's a quick reference to show just how tight the financial requirements are for applicants.

| Metric | Federal Guideline / State Example | What It Means for You |

|---|---|---|

| Individual Asset Limit | $2,000 | This is the maximum value of countable assets a single applicant can own to qualify. |

| Community Spouse Resource Allowance (CSRA) | Up to $157,920 | This is the amount of assets the healthy spouse can keep to avoid impoverishment. |

| Monthly Maintenance Needs Allowance (MMNA) | $2,555 – $3,853.50 | The range of monthly income the community spouse is allowed to keep. |

| Home Equity Limit | $713,000 – $1,071,000 | The maximum equity you can have in your primary residence and still have it be an exempt asset. |

Note: These figures are based on federal guidelines and can vary by state. Always verify the current numbers for your specific location.

As you can see, the numbers are unforgiving for a single applicant but provide crucial protections when a spouse is still living at home.

Protections for the Community Spouse

So, what happens if one spouse needs to go into a nursing home, but the other is still living independently at home? Thankfully, the system has built-in protections to prevent the "community spouse" from being left with nothing. This is where the Community Spouse Resource Allowance (CSRA) becomes so important.

The CSRA is a critical lifeline. It allows the healthy spouse to keep a significant chunk of the couple's joint assets, ensuring they aren’t forced into poverty just because their partner needs long-term care.

While the applicant spouse is still held to that $2,000 asset limit, the at-home spouse can keep far more. The CSRA amount for 2025 can be as high as $157,920 under federal guidelines. This rule is fundamental to how Medicaid tries to balance providing essential care with protecting the financial security of the healthy spouse.

On top of the CSRA, the community spouse might also be able to keep a portion of the institutionalized spouse's income. This is called the Monthly Maintenance Needs Allowance (MMNA), and it’s designed to make sure the at-home spouse has enough income to actually live on. Understanding these spousal protections is a cornerstone of smart planning and can make all the difference in preserving a couple's financial legacy.

Using Trusts for Asset Protection

When it comes to protecting your assets from nursing home costs, trusts are the single most powerful tool in the playbook. I’ve seen them work wonders for families, but it’s critical to understand that not just any trust will do.

Many people have a revocable living trust as part of their estate plan, and they assume it shields their assets. Unfortunately, for Medicaid purposes, it does absolutely nothing. Because you can change or cancel a revocable trust at any time, Medicaid sees those assets as completely yours and, therefore, "countable."

To get real protection, you need a very specific tool: an irrevocable trust designed for this exact purpose.

The Irrevocable Trust: The Gold Standard

Unlike its revocable cousin, an irrevocable trust is a serious, legally binding arrangement. Once you create it, you generally can’t change or undo it.

When you transfer assets—like your home or an investment portfolio—into this type of trust, you are legally giving up direct ownership and control. This is the secret sauce that makes it so effective.

From Medicaid's perspective, assets held in a properly structured irrevocable trust are no longer considered yours. They don't count toward that strict $2,000 asset limit, and they’re safe from Medicaid Estate Recovery after you pass away. It is the definitive way to preserve your life savings for your spouse, children, or other heirs.

But let me be clear: this is not a DIY project. An irrevocable trust is a complex legal document. It absolutely must be drafted by an experienced elder law attorney to ensure it complies with your state’s specific rules and doesn't accidentally disqualify you.

Meet the Medicaid Asset Protection Trust (MAPT)

The go-to irrevocable trust for this strategy is the Medicaid Asset Protection Trust (MAPT). Think of it as a secure legal vault for your most important assets. You, the "grantor," create the trust and place your assets inside. Then, you name someone you trust—often an adult child—as the "trustee" to manage those assets according to the rules you’ve laid out.

The beauty of a MAPT is the balance it strikes. You get incredible protection without having to give up all the perks of your assets.

- You can still get the income. The trust can be written so that you continue to receive any income the assets generate, like stock dividends or rent from a property.

- You can live in your home. If you put your primary residence into a MAPT, you can retain the legal right to live there for the rest of your life. No questions asked.

- You can keep your tax benefits. You still get to claim property tax exemptions like STAR or a veteran’s exemption. Just as important, your heirs get a "step-up" in basis on the home's value when you pass away, which can save them a fortune in capital gains taxes if they decide to sell.

The core principle is simple: the trustee controls the principal (the assets themselves), while you can still benefit from the income and use of the property. This separation is what shields the assets from being counted by Medicaid.

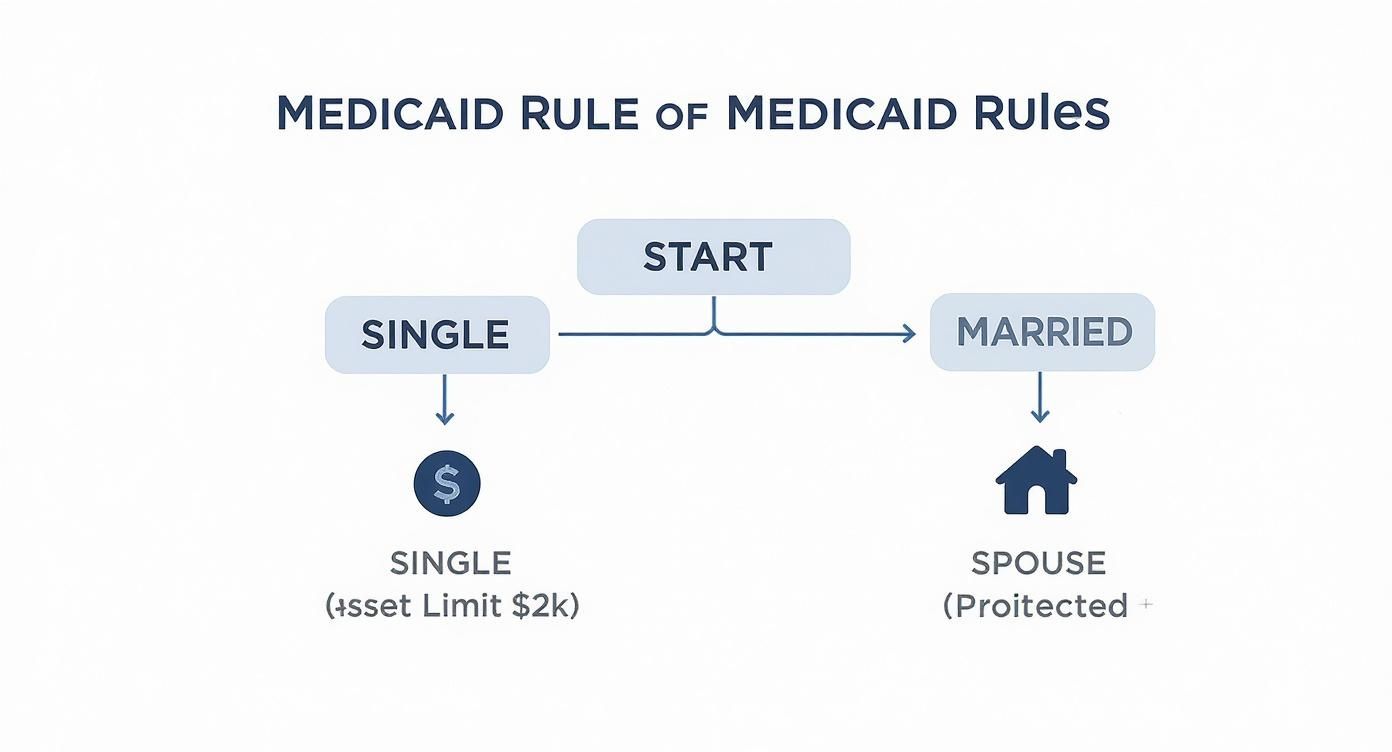

This decision tree shows how Medicaid's rules differ based on marital status, highlighting why spousal protections are so critical.

As the infographic shows, a single individual faces a very low asset limit. But the rules provide significant allowances to protect the financial stability of a spouse who remains at home.

A Real-World MAPT Example

Let’s walk through a common scenario. Imagine John and Mary, both 68 years old. Their main assets are their home, valued at $450,000, and about $200,000 in a brokerage account. They're healthy now but are smart enough to plan ahead.

They meet with an elder law attorney and create a Medicaid Asset Protection Trust. They name their responsible daughter, Sarah, as the trustee. They then formally deed their home to the trust and transfer the brokerage account into it as well.

Here’s what this single move accomplishes:

- Ownership is transferred. Legally, John and Mary no longer own the house or the investments. The trust does.

- They retain control over daily life. They continue to live in their house just as they always have, paying the property taxes and utilities. Nothing changes for them day-to-day.

- Income still flows to them. Any dividends from the brokerage account are paid directly to John and Mary, which they can use for their living expenses.

- The principal is protected. As trustee, Sarah manages the investments for the trust's long-term health. She cannot give the principal back to her parents (as that would break the trust's protection), but she can ensure it grows for the future.

Now, let's fast forward six years. John has a stroke and needs to move into a nursing home. When Mary applies for Medicaid on his behalf, the $650,000 in assets held within the MAPT are completely invisible to Medicaid. Because they are well outside the five-year look-back period, John can qualify for benefits almost immediately.

They didn't have to spend down their life savings. The house is safe, the investments are protected for Mary and Sarah, and the legacy they worked their whole lives to build is secure.

Legal Strategies Beyond Trusts

While an irrevocable trust is a powerful tool for long-term planning, it's certainly not the only one. A good elder law attorney has a whole toolkit of strategies to protect your assets, especially when a crisis hits and you're suddenly inside that five-year look-back period.

These methods are all about legally converting assets that Medicaid can count against you into assets that it can't. It’s what we call "crisis planning"—for families who suddenly find themselves needing nursing home care right now, without the luxury of years to prepare. It’s a stressful spot to be in, but it’s crucial to know that you still have powerful options.

Using Medicaid Compliant Annuities

One of the most effective tools for a crisis situation is the Medicaid Compliant Annuity. This isn't the kind of annuity you buy for investment growth. It’s a highly specialized financial product designed to do one thing very well: take a large chunk of countable cash and turn it into a non-countable income stream, practically overnight.

Here’s a real-world scenario. Imagine David, a single man, has a sudden stroke and needs to move into a nursing home. He has $150,000 in savings, which is way over the $2,000 asset limit for Medicaid. The nursing home costs $12,000 a month. Instead of just paying that rate until his savings are gone, his family works with an attorney.

They purchase a Medicaid Compliant Annuity. This isn't just any annuity; it has very strict rules:

- It must be irrevocable (you can't undo it) and non-assignable (you can't sell it).

- It must pay out in equal monthly payments.

- The payback term has to be shorter than the owner's official life expectancy.

- The state’s Medicaid agency must be named the primary beneficiary if the owner passes away before the annuity is fully paid out.

By buying this annuity, David’s $150,000 in countable assets is instantly gone. It’s now an income stream that helps pay for his care, but that lump sum no longer disqualifies him from Medicaid. He can get the benefits he needs much sooner, protecting a huge portion of his life savings that would have otherwise vanished.

The Power of Strategic Gifting

Giving money to your kids might seem like an easy way to lower your assets, but if you do it wrong, you could face a devastating Medicaid penalty period. But there is a right way to do it.

The key is to understand how the penalty is calculated. It’s the total amount you gifted divided by the average monthly cost of care in your state. A skilled attorney might advise making a very specific, calculated gift that creates a known penalty period. During that time, the family uses other funds to pay for care. As soon as that penalty period is over, the person can qualify for Medicaid, having successfully passed that gift on to their heirs.

This strategy is like a carefully planned chess move. It’s not about just giving money away; it’s about timing the gift and the penalty period to maximize the amount of assets preserved while still ensuring continuous care.

Of course, none of these strategies work if you don't have your foundational essential estate planning documents in place. A durable Power of Attorney is absolutely critical, as it allows a trusted person to execute these plans if you can't. Understanding the difference between a power of attorney and guardianship is the first step.

Legal Spend-Down Strategies

When you have to reduce your assets to qualify for Medicaid, most people think their only option is to write checks to the nursing home until the money runs out. That’s simply not true. The "spend-down" process lets you spend money on things that benefit you or your spouse, as long as you get fair market value for it.

Instead of just watching your savings get eaten up by the facility's monthly bill, you can legally spend that money on other things you actually need.

Here are a few smart and effective ways to spend down assets:

- Pay Off Debts: You can wipe out a mortgage, pay off a car loan, or clear all your credit card balances. You're turning a cash asset into valuable debt relief.

- Home Repairs and Modifications: This is a big one. You can make your home safer and more accessible by adding a ramp, renovating a bathroom, or even putting on a new roof.

- Purchase a New Vehicle: If your car is on its last legs, buying a new, reliable one is a perfectly allowable spend-down expense.

- Pre-Pay Funeral Expenses: Setting up an irrevocable funeral trust is a common and wise strategy. It’s a non-countable asset, and it relieves your family of a huge burden down the road.

This is all about being strategic. You're not just draining a bank account. You're using those funds to pay off obligations, improve your quality of life, and secure your spouse's future—all while moving yourself closer to Medicaid eligibility.

How to Protect Your Primary Home

For most of us, our home is so much more than just a financial asset. It’s the heart of the family, a place filled with memories. Making sure it’s safe from the staggering costs of long-term care is usually the top priority for our clients.

Here's a common and dangerous misconception: many people believe that because their primary residence is an "exempt" asset for Medicaid eligibility, it's safe. While it's true you won't be forced to sell your home to qualify for Medicaid (as long as you or your spouse live there), that protection is temporary and misleading.

The real danger comes later, in the form of Medicaidaid Estate Recovery. After a Medicaid recipient passes away, the state essentially becomes a creditor. It will come looking to get paid back for every dollar it spent on your care, and the family home is often the only valuable asset left to satisfy that debt.

This means your home could be forced into a sale after you're gone, leaving your heirs with nothing. Thankfully, there are powerful and proven legal strategies to make sure this doesn't happen.

Transferring Your Home to an Irrevocable Trust

By far, the strongest and most secure way to protect your home is to transfer it into a Medicaid Asset Protection Trust (MAPT). As we've touched on before, this move legally takes the house out of your name. It effectively builds a wall around the property, putting it beyond the reach of both nursing homes and the state's recovery efforts.

When you deed your home to a MAPT, you don't lose the ability to live in it. The trust document is drafted to include a right of occupancy, which guarantees you can live there for the rest of your life. For all intents and purposes, nothing about your daily life changes—but your home is now completely secure.

The key is planning ahead. This transfer has to happen at least five years before you apply for Medicaid to avoid running afoul of the look-back period. It truly is the gold standard for protecting your home.

Using a Life Estate Deed

A Life Estate deed is another tool we sometimes use, though it comes with some serious trade-offs and offers less protection than a trust. The setup is simple: you transfer ownership of your home to your children (who are called the "remaindermen") but keep a "life estate" for yourself. This gives you the legal right to live there until you die.

When you pass away, the home automatically transfers to your children, bypassing both the probate process and Medicaid Estate Recovery. It sounds great on the surface, but you need to be aware of the risks involved.

- You Give Up Control: Once that deed is signed, you can't just sell or mortgage the property on your own. You need every single one of the remaindermen to agree and sign off.

- Their Problems Become Your Problems: If one of your children gets divorced, files for bankruptcy, or gets hit with a lawsuit, your home could suddenly be considered their asset and be at risk from their creditors.

- Potential Tax Headaches: This strategy can create some complicated capital gains tax issues for your children when they eventually decide to sell the property.

A Life Estate can work in very specific, straightforward situations, but it just doesn't have the flexibility or the bulletproof protection of a properly drafted irrevocable trust.

Leveraging Powerful Exemptions

Beyond trusts and deeds, federal law has carved out a few narrow but incredibly powerful exemptions. These are the exceptions that allow you to transfer a home without penalty, even if you're inside the five-year look-back period. They can be an absolute lifesaver in a crisis situation.

The most significant of these is the Child Caregiver Exemption. This is a little-known rule that can be a game-changer for families where an adult child has stepped up to care for an aging parent at home.

The Child Caregiver Exemption lets you transfer your home to an adult child without triggering a Medicaid penalty, but only if that child meets two very strict conditions:

- They had to have lived in the home with you for at least two years right before you moved to a nursing home.

- The care they gave you during that time was essential and was the reason you were able to delay moving into a facility.

Think about it: a daughter moves back home to care for her aging mother. For two and a half years, she helps with meals, bathing, and medications. When her mother's health finally declines to the point where a nursing home is necessary, the house can be legally transferred into the daughter's name. This one move saves the family's most cherished asset from being sold off, all while rewarding the daughter for her years of sacrifice and care.

Answering Your Biggest Asset Protection Questions

When you're thinking about long-term care, the questions can feel overwhelming. The fear of making a wrong move, tangled up with all the legal jargon, can be paralyzing. Let's cut through that confusion and tackle the most common worries we hear from families just like yours.

Is It Too Late to Protect Assets if My Parent Already Needs Care?

This is easily the most urgent question we get, and the answer is almost always no, it's not too late. It’s true that planning five years ahead gives you the most options. But even if your loved one is on the brink of needing nursing home care, there are powerful crisis planning strategies we can use.

An experienced elder law attorney has specific tools, like Medicaid Compliant Annuities or certain promissory notes, that can shield a large chunk of a family's savings. The most important thing is to act fast and get professional help. Don't ever assume it's a lost cause just because a health crisis has struck.

Will I Lose Control If I Put My House in a Trust?

That's a completely fair question. Nobody wants to feel like a guest in their own home. The good news is, a properly drafted trust is built to protect you, not take away your power. When your home goes into what's called a Medicaid Asset Protection Trust (MAPT), you absolutely can—and should—keep the right to live there for the rest of your life.

This is formally written into the trust as a "right of occupancy." It means your trustee, who might be one of your kids, has no power to sell the house from under you or kick you out. You go on living in your home, paying the bills, and enjoying it like you always have. The only difference is that its value is now safely protected for your family down the road.

A big myth is that an "irrevocable" trust means you've lost all control. The reality is, you're the one who sets the rules from the start. You can keep the right to live in your home and even change who inherits it, all while the asset itself is shielded.

Can I Just Give My Money to My Kids?

This is probably the most common—and most damaging—mistake we see families make. Just writing a big check to your children to get your assets under the Medicaid limit is almost guaranteed to backfire. Any gifts or transfers made for less than what they're worth within the five-year look-back period will bring on a penalty.

Medicaid calls this an "uncompensated transfer" and will hit you with a period of ineligibility. That means Medicaid will flat-out refuse to pay for care for a number of months, or even years, depending on how much money was given away. This leaves your family in a terrible spot, forced to pay for expensive care out-of-pocket, often long after that gifted money has been spent.

What Happens to My IRA or 401(k)?

Retirement accounts are tricky, and the rules can be wildly different from one state to the next. In many areas, an IRA or 401(k) that belongs to the person applying for Medicaid is considered a countable asset, especially if they’re taking regular payments from it.

But the rules often change for the "community spouse" (the one who's not in the nursing home). Their retirement accounts are usually protected and don't count against their spouse's eligibility. For the person needing care, strategies might involve a planned spend-down to pay for care during a penalty period or moving the funds into a Medicaid Compliant Annuity. This is a very technical area where getting state-specific advice from an elder law attorney is non-negotiable if you want to avoid a costly mistake.

At NJ Caregiving, we understand that navigating these challenges is stressful. Our dedicated team provides compassionate in-home care to support your family every step of the way. If you need support for a loved one in Mercer County, visit us online to learn how we can help.