Yes, Medicare covers some types of home care, but here's the catch every family needs to know: it’s strictly for short-term, skilled medical care after an illness, injury, or hospital stay. It is not designed to pay for long-term personal help with daily activities like bathing, dressing, or making meals.

What Medicare Home Care Really Covers

Trying to figure out Medicare's home care benefits can feel like trying to assemble furniture with the instructions in another language. Many families are caught by surprise when they learn that Medicare won't cover a full-time aide to help with daily life. This is one of the most common—and costly—misconceptions out there.

The key is getting your head around Medicare's very specific definition of "home health care."

Think of this benefit less as a long-term support system and more as a temporary medical bridge. Its entire purpose is to help a senior recover from an acute event—like surgery or a serious injury—in the comfort of their own home. It provides the necessary medical services to get them back on their feet, not to assist with ongoing daily needs.

The Critical Difference: Skilled vs. Custodial Care

The most important distinction to grasp is between skilled care and custodial care. Medicare's home health benefit is built entirely around the first one and flat-out excludes the second. This single difference determines everything that is and isn’t covered.

-

Skilled Medical Care (This is what Medicare covers): These are services that can only be safely and effectively performed by a licensed health professional, or under their direct supervision. Think of things like physical therapy to regain mobility after a fall, wound care from a registered nurse, or speech therapy following a stroke.

-

Custodial Care (This is what Medicare does NOT cover): This is all about non-medical help with Activities of Daily Living (ADLs). It includes hands-on assistance with bathing, dressing, eating, using the bathroom, and preparing meals. While absolutely essential for many seniors, Medicare doesn’t classify this as "medical" care, so it doesn't pay for it.

Medicare focuses on medically necessary, intermittent care that actively treats an illness or injury. It was never intended to be a solution for chronic, long-term assistance with personal tasks.

To make this crystal clear, here’s a simple breakdown of the services that typically fall under each category.

Medicare Home Health At a Glance: Skilled vs. Custodial Care

| Service Type | Usually Covered by Medicare (Skilled Care) | Usually Not Covered by Medicare (Custodial Care) |

|---|---|---|

| Personal Care | Bathing/dressing only if part of skilled care plan | Bathing, dressing, grooming, and toileting assistance |

| Medical Services | Part-time skilled nursing, physical/occupational/speech therapy | Medication reminders (unless part of a skilled care plan) |

| Household Help | None | Meal preparation, shopping, laundry, and light housekeeping |

| Companionship | None | Social interaction, supervision, and escorting to appointments |

| Care Schedule | Intermittent (part-time, for a limited duration) | 24-hour care, long-term or ongoing assistance |

This table helps you see at a glance why a doctor might order skilled nursing visits, but Medicare won't approve a request for someone to help with laundry and cooking.

A Growing Need for In-Home Services

The demand for these services is climbing, and fast. Over the past decade, the use of home health care has been on a steady rise. In 2020 alone, there were approximately 424 million home health care visits in the U.S., which is a 7.6% increase from 2013.

Medicare is the biggest single payer for these services, covering about 42% of all home health visits. This shows just how vital its role is in helping seniors recover at home. You can read more about these trends and the growing reliance on home health care to see how the landscape is changing.

Understanding this framework right from the start will help you set realistic expectations and create a more effective care plan for your loved one’s complete needs.

Meeting the Eligibility Criteria for Home Care

Qualifying for Medicare's home health benefits isn't as simple as just needing a little help around the house. It’s a very specific process with a clear set of medical rules. Think of it like a combination lock—you have to get every number right for it to open.

Medicare’s goal is to ensure the home care for seniors Medicare covers is truly for medical recovery from an illness or injury. If even one piece of the puzzle is missing, a claim can be denied. Let's walk through exactly what you'll need to have in place.

The Doctor's Certification and Plan of Care

It all starts with your doctor. A physician must formally certify that you have a medical need for skilled care in your home. This isn’t a casual note; it’s an official determination that kicks off the entire process. Part of this involves documenting a recent face-to-face visit where your condition was discussed.

From there, your doctor will collaborate with a Medicare-certified home health agency to create a plan of care. This is your roadmap to recovery. It lays out everything in detail, including:

- The skilled services you require (like nursing or physical therapy).

- How often the professionals will visit.

- Any medical equipment you'll need, such as a walker.

- The specific treatment goals.

This plan isn't set in stone. Your doctor is required to review and re-certify it at least every 60 days to make sure the care is still necessary and helping you progress.

The Homebound Requirement Explained

The term "homebound" trips a lot of people up. It sounds like you have to be stuck in bed 24/7, but that's not the case at all. Medicare’s definition is actually much more practical than most families realize.

To be considered homebound, leaving your home must take a "considerable and taxing effort." This is usually because an illness or injury makes it physically difficult to get around.

So, what does that look like in real life? You can still be homebound and go to doctor's appointments, religious services, or even an adult day care program. An occasional short trip, like getting a haircut, is usually fine too. The main point is that leaving home is a significant challenge that requires help from someone else or a device like a wheelchair or walker. For a deeper dive, check out our guide on Medicare home health requirements.

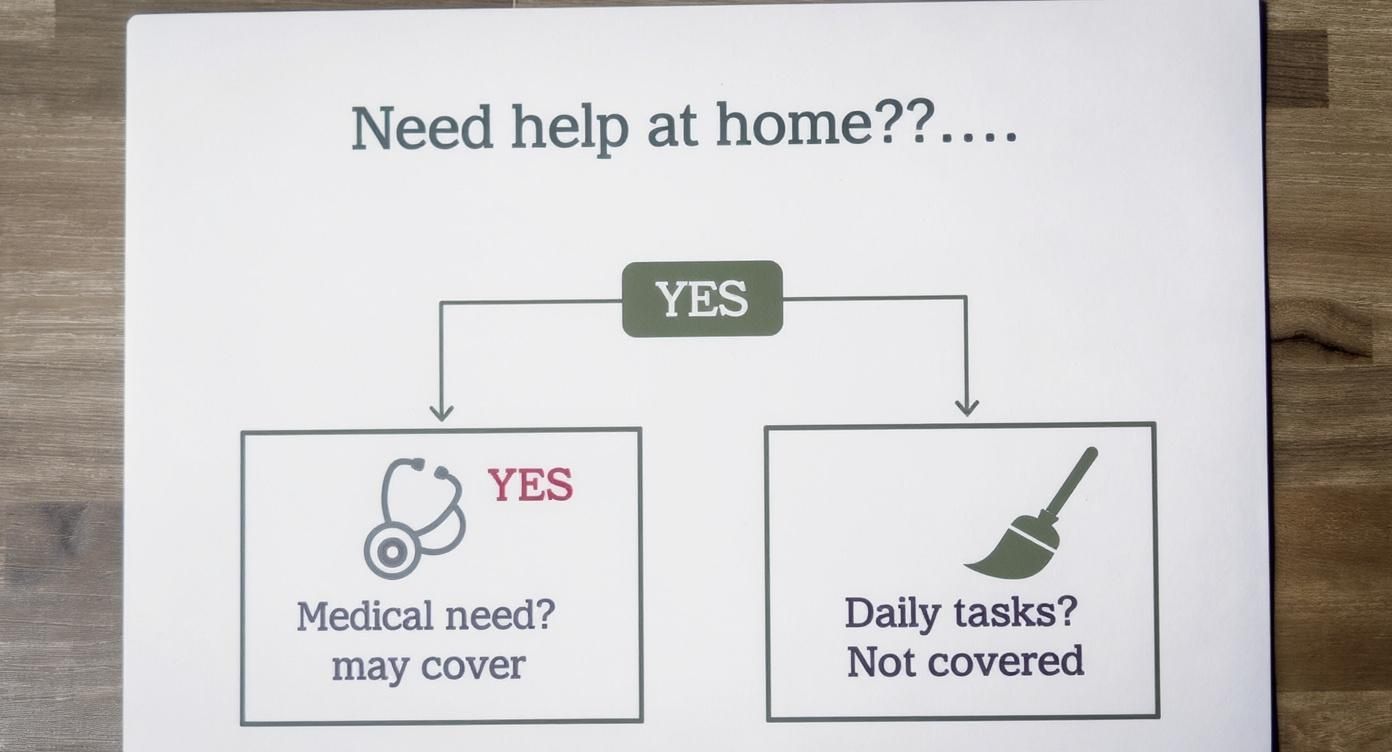

This flowchart helps visualize the difference between the medical care Medicare covers and the personal care it generally doesn't.

As you can see, the path to coverage always starts with a medical need, separating it from general help with daily activities.

Proving the Need for Skilled Services

The last key piece is demonstrating a need for intermittent skilled care. In plain English, this means you need part-time services from a licensed healthcare professional.

To qualify, you must need at least one of these:

-

Intermittent Skilled Nursing Care: This covers tasks performed by a registered nurse (RN) or licensed practical nurse (LPN), like wound care, managing IVs, or injections. The care has to be needed fewer than 7 days a week or less than 8 hours per day.

-

Physical Therapy (PT), Speech-Language Pathology (SLP), or Occupational Therapy (OT): If you need therapy to recover from an injury or prevent your condition from getting worse, this can be your sole qualifying reason for Medicare home health benefits.

It's important to know that once you qualify with a need for nursing or therapy, Medicare might also pay for a home health aide. An aide can help with personal tasks like bathing and dressing. However, needing help with personal care alone is not enough to qualify. It's an add-on service, not the main event. Meeting all these criteria ensures your care plan aligns with Medicare's focus on short-term, skilled recovery at home.

A Deep Dive into Covered Services

Once your doctor gives the green light and confirms you're eligible, the next big question is always the same: what does Medicare home care actually involve? It helps to think about these services in real-world terms, not just as a checklist.

At its core, Medicare's home health benefit is all about bringing skilled, medically necessary care right to your doorstep. These aren't just everyday tasks; they're services that require a licensed professional to help you recover from an illness or injury. Think of it as a short-term bridge to get you back on your feet, not a permanent care solution.

Part-Time or Intermittent Skilled Nursing Care

One of the most common services you’ll see is skilled nursing care, but it’s delivered on a part-time or "intermittent" basis. This is a key phrase. It means care is provided for fewer than eight hours a day and not every single day of the week, ensuring it remains focused on specific medical needs.

So, what does a skilled nurse actually do during a visit? They’re there to handle the medical tasks laid out in your doctor's care plan.

- Wound Care: If you're recovering from surgery, a nurse might visit to properly clean and dress a wound, keeping a close eye out for any signs of infection.

- IV Therapy: Administering medications or fluids through an IV is a delicate task that requires a licensed pro.

- Injections: A nurse can handle necessary injections, like insulin, for patients who can't safely do it themselves.

- Patient and Caregiver Education: This is a huge one. A great nurse will teach you and your family how to manage the condition, from medication schedules to spotting potential warning signs.

The nurse’s role is purely medical and goal-oriented. They aren't there to help with housekeeping or meals; their focus is entirely on your health and recovery.

Restorative Therapies

Right alongside nursing care, you have rehabilitative therapies. These are the services designed to help you regain function, improve your mobility, and reclaim your independence after something like a fall, a stroke, or a major surgery.

The great thing is, you can qualify for home health care if you need any of these therapies, even if you don't need a nurse at the same time.

- Physical Therapy (PT): A physical therapist works to restore your strength, balance, and movement. After a hip replacement, for example, a PT would guide you through exercises at home to help you walk, climb stairs, and get out of a chair safely.

- Occupational Therapy (OT): An occupational therapist is all about helping you get back to performing daily activities. They might show a stroke survivor new ways to get dressed or help adapt the home by adding grab bars in the bathroom to make it safer.

- Speech-Language Pathology (SLP): Often just called speech therapy, these services help with communication or swallowing problems that can pop up after a stroke or another neurological event.

The whole point of therapy is progress. Your therapist will work with you to set and hit specific goals, with the ultimate aim of helping you become as self-sufficient as possible in your own home.

Other Essential Covered Services

Once you qualify for skilled nursing or therapy, Medicare might also cover a few other vital support services as part of your overall care plan.

- Home Health Aide Services: If you're receiving skilled care, a home health aide may also be approved to help with personal tasks like bathing, dressing, or using the bathroom. But here's the catch: needing personal care alone won't qualify you. It’s an add-on service, not a standalone benefit.

- Medical Social Services: A social worker can be a lifeline, helping you and your family navigate the emotional and social hurdles of an illness. They can connect you to fantastic community resources like meal delivery programs or local support groups.

- Durable Medical Equipment (DME): Medicare Part B will typically cover 80% of the cost for necessary medical equipment like walkers, wheelchairs, or hospital beds. You would be responsible for the remaining 20% coinsurance.

Getting a handle on the full scope of these benefits is key. Our comprehensive guide on Medicare home health benefits digs even deeper into how all these services work together.

It's also interesting to see how these benefits are being used. For instance, home health care for Medicare beneficiaries with dementia is on the rise. Between 2010 and 2019, use increased from 35.4 to 40.2 spells per 1,000 beneficiaries, which really shows a growing understanding of how valuable this kind of support can be. This trend underscores just how important it is to have a cohesive care plan that pulls all these covered services together.

Understanding Your Costs with Medicare

For most families, the practical question always comes down to money: “What is this actually going to cost?” When you’re trying to arrange home care for seniors medicare is a huge help, but understanding the out-of-pocket expenses is just as crucial as knowing what services are covered.

The good news is that for eligible seniors, Original Medicare makes home health care remarkably affordable.

If you meet all the criteria and use a Medicare-certified home health agency, Original Medicare (Part A and Part B) pays 100% for your covered home health services. That means you’ll have $0 in copayments or deductibles for skilled nursing visits and therapy sessions. This is a massive relief for families managing a loved one's recovery after a hospital stay.

However, there’s a potential cost that can sometimes catch people by surprise.

The Cost of Durable Medical Equipment

While your skilled nursing and therapy visits are fully covered, there's a different rule for any necessary durable medical equipment (DME). This includes things like walkers, hospital beds, wheelchairs, or oxygen equipment that your doctor orders for use at home.

Under Original Medicare, once you’ve met your annual Part B deductible, Medicare will pay for 80% of the approved amount for your DME. You are responsible for the remaining 20% coinsurance. For example, if you need a specialized walker that costs $100, Medicare would cover $80, leaving you to pay the remaining $20.

This is a common point of confusion. The skilled services are covered at 100%, but the equipment you need for recovery falls under the standard 20% coinsurance rule of Medicare Part B. It's always a good idea to clarify this with your home health agency upfront.

Original Medicare vs. Medicare Advantage Plans

The cost structure can change quite a bit if you’re enrolled in a Medicare Advantage (MA) plan, also known as Part C. These are private insurance plans, and while they must cover everything Original Medicare does, they have their own rules, networks, and cost-sharing structures.

Medicare Advantage plans have become a dominant force in senior healthcare. In fact, it's projected that more than half (54%) of all eligible beneficiaries will be enrolled in an MA plan in 2025. While home health usage is nearly identical between MA plans and Original Medicare, the financial experience can be very different. You can learn more about these Medicare Advantage trends on KFF.org to understand their growing impact.

Here's how Medicare Advantage plans often differ:

- Provider Networks: Most MA plans have a specific network of doctors and home health agencies. Going "out-of-network" can mean much higher costs or no coverage at all.

- Prior Authorization: You may need to get approval from your plan before home health care can begin, which can sometimes cause delays.

- Copayments: Unlike Original Medicare's $0 cost, some MA plans might charge a copayment for each home health visit.

Key Questions to Ask Your Plan Administrator

If you have a Medicare Advantage plan, you have to be your own best advocate. Don't assume the rules are the same as Original Medicare. Before starting care, grab the phone, call your plan's administrator, and ask these specific questions to avoid financial surprises down the road.

-

Is this home health agency in my plan’s network?

This is the most critical first step. Using an out-of-network agency could leave you with a substantial bill. -

Do I need prior authorization for these services?

Find out what paperwork is needed and how long the approval process usually takes. This can prevent frustrating delays in starting care. -

Will I have a copayment for each skilled nursing or therapy visit?

Get a clear dollar amount so you can budget for it. -

What are my costs for durable medical equipment?

Confirm your coinsurance or copay for items like walkers or bedside commodes.

Asking these direct questions gives you a clear picture of your financial responsibilities, ensuring the home care for your loved one is both effective and affordable.

How to Find a Medicare-Certified Agency

Once you know your loved one is eligible for home care covered by Medicare, the next big step is finding the right partner for their recovery. This isn’t just about hiring any agency; it's about finding a high-quality, Medicare-certified team you can trust with their health and well-being.

Choosing an agency can feel like a huge task, but thankfully, Medicare has an excellent tool to help you make a smart, informed decision. It's designed to give you an objective look at providers based on real quality metrics and patient feedback.

Using Medicare's Care Compare Tool

Think of Medicare's official Care Compare tool as your research starting point. This online database gives you a transparent look at how different home health agencies are performing. It makes it easy to search for providers in your area and see exactly how they stack up.

Using the tool is simple. Just pop in your location, and it will pull up a list of Medicare-certified agencies nearby. For each one, you’ll find crucial information that paints a clear picture of their service quality.

The tool provides two key ratings that are especially helpful:

- Quality of Patient Care Star Rating: This is an overall score, from one to five stars, based on how well an agency manages daily activities, prevents hospital readmissions, and handles other key care measures.

- Patient Survey Star Rating: This rating comes directly from what actual patients have said about their experiences, covering everything from communication to the professionalism of the staff.

An agency's star ratings give you a valuable, at-a-glance summary of its performance. While a five-star rating is a great sign, don't automatically rule out agencies with slightly lower scores. Use the ratings to build a shortlist, then dig deeper with your own questions.

Your Checklist for Vetting Agencies

After using the Care Compare tool to find a few promising options, it’s time to pick up the phone. An interview is your chance to get a feel for an agency's culture, their processes, and how committed they are to patient care. Remember, you’re not just hiring a service; you're inviting people into your home during a very personal and often vulnerable time.

Here are the essential questions you should ask every potential agency to make sure they're the right fit for your family.

Staff Qualifications and Training

The skill and compassion of the caregivers are the heart of any good home health agency. You need to feel confident that the professionals walking through the door are well-qualified and ready for anything.

- Are all your caregivers licensed, bonded, and insured? This is non-negotiable. It protects both the patient and your family from any liability.

- What kind of background checks do you perform? Make sure they conduct thorough national criminal background checks on all staff.

- What ongoing training do your nurses and therapists receive? Healthcare is always changing, and the best agencies invest in continuous education for their teams.

Care Coordination and Communication

Great communication is the glue that holds a care plan together. You want an agency that works seamlessly with your loved one's doctor and keeps your family in the loop every step of the way.

- How will you coordinate with my loved one’s primary care physician? Ask them to walk you through their process for sharing updates on progress or any changes in condition.

- Who is our main point of contact at the agency? There should be a dedicated case manager or coordinator you can easily reach with questions.

- How do you handle after-hours emergencies or questions? Confirm they have a clear protocol in place, including an on-call nurse who is available 24/7.

A clear communication plan from day one prevents misunderstandings and makes sure everyone is on the same page, which is absolutely critical for effective home care for seniors medicare plans. Taking the time to ask these questions will empower you to choose an agency with confidence, knowing you’ve found a reliable partner for your loved one’s recovery journey.

Filling the Gaps in Medicare Coverage

Let’s be clear about what Medicare’s home health benefit is designed for. It’s a short-term, skilled medical service. Think of it as a specialized crew that visits after a hospital stay to handle things like wound care, IV therapy, or physical therapy. They’re experts in medical recovery, but their job isn't to stick around and help with the daily ins and outs of life once the immediate health crisis has passed.

This creates a pretty significant gap for many families. What happens when Mom or Dad is medically stable but still can’t safely get dressed, make a meal, or needs someone around for companionship? This is where the non-medical, daily support tasks come into play—the very things Medicare wasn’t built to cover.

The best approach is often to blend Medicare's skilled benefits with private-pay services to create a complete safety net that addresses a senior's total well-being.

Building a Comprehensive Care Plan

A truly supportive care plan starts by understanding what Medicare provides and then intentionally filling in the missing pieces. You have Medicare’s team handling the skilled nursing and therapy to get your loved one back on their feet. At the same time, your private-pay team—like the caregivers from NJ Caregiving—steps in to manage everything else.

This creates a seamless circle of care. A Medicare-funded nurse might visit a few times a week, but a private-duty aide can be there every day to help with personal care, prevent falls, and make sure they’re eating well. These are the critical factors that often make or break a successful recovery. The two teams work in parallel: one focused on medical healing, the other on daily comfort and safety.

A common mistake families make is assuming that when Medicare services stop, the need for help is over. In reality, the end of skilled care is often when the need for personal support becomes most obvious.

What Private-Pay Services Can Provide

Private-duty home care, which is sometimes called custodial care, is designed to cover exactly what Medicare doesn’t. It’s the key to helping someone maintain their independence and quality of life at home for the long haul.

These services usually include:

- Personal Care: Providing dignified help with bathing, dressing, grooming, and using the bathroom.

- Meal Preparation: Planning and cooking healthy meals to support recovery and overall health.

- Companionship: Offering social interaction and a friendly face to combat the loneliness that can creep in.

- Light Housekeeping and Errands: Helping with laundry, grocery runs, and keeping the home safe and tidy.

To get a really clear picture of how these roles differ, take a look at our article that digs into whether https://njcaregiving.com/will-medicare-pay-for-a-home-health-aide/.

When you realize Medicare won't cover everything, it's wise to explore other funding options. Understanding the key differences between government programs is a great place to start. Resources that compare Medicare vs. Medicaid for Senior Care can give you valuable insight into other ways to get financial help. This blended approach—combining home care for seniors medicare benefits with private support—creates the strong, reliable system your loved one needs to thrive safely at home.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following the provided style guide.

Your Medicare Home Care Questions, Answered

When you’re trying to figure out home care for seniors through Medicare, a lot of specific questions pop up. It’s completely normal. Here are some straightforward answers to the things we hear most often from families, designed to give you clarity and confidence.

Can I Get Home Care if I Live in an Assisted Living Facility?

Yes, absolutely. Many people don't realize this, but you can still get Medicare-covered home health services even if you live in an assisted living community. As long as that facility is considered your "home" and you meet the other eligibility rules, Medicare will cover those skilled services.

The key thing to remember, though, is that Medicare will not pay for the costs of the facility itself, like your room and board.

Is There a Time Limit on How Long I Can Receive Care?

This is a big one, and the answer is no—there’s no lifetime limit on Medicare home health care. The benefit isn't about a fixed number of days; it’s all about your ongoing medical need.

Your care is structured in 60-day periods, which you’ll often hear called "episodes of care." As long as you still meet the requirements, your doctor can simply re-certify your plan of care for another 60 days, and this can continue as long as necessary.

What Happens if My Condition Gets Better?

If your health improves and you no longer need skilled nursing or therapy, or you're not considered homebound anymore, the home health agency will start planning for your discharge. They are required to give you a formal written notice at least two days before services end.

This notice isn't just a heads-up; it will clearly explain why they're ending services and give you instructions on how you can appeal the decision if you don't agree.

Sorting through these details is so much easier when you have a partner you can trust. NJ Caregiving is here to help fill the gaps that Medicare doesn't cover, creating a complete circle of support for your loved one. To see how our compassionate caregivers can help them live comfortably and safely at home, visit us at https://njcaregiving.com.