Yes, Medicare can pay for a home health aide, but this is one of the most misunderstood benefits out there. The rules are very specific and narrow. It’s absolutely critical to understand that this isn’t a long-term solution for daily help. Instead, think of it as short-term support directly tied to your recovery from an illness or injury, all under a doctor's close supervision.

Understanding Medicare's Home Health Aide Coverage

When you hear "home health aide," you probably picture a kind person helping with daily chores, cooking, and providing companionship. That's a common and understandable image, but it's not what Medicare’s benefit is designed for.

Medicare's coverage is more like a temporary bridge to recovery, not a permanent support system for daily living.

The main purpose is to provide personal care—that means hands-on help with activities like bathing, dressing, and using the bathroom—but only while you are also getting skilled medical care. The aide’s services have to be part of a larger, doctor-prescribed plan of care.

Key Conditions vs. Common Misconceptions

Let's clear up the confusion right away. Many families assume Medicare will send an aide to help with everyday life, but the requirements are much, much stricter. The aide's role is solely to support a medical recovery plan.

Medicare will not pay for custodial or personal care that helps you with daily living activities when this is the only care you need. The aide's services must be combined with skilled nursing or therapy.

This single point is the biggest hurdle and the most frequent source of denied claims. If a doctor hasn't certified a medical need for skilled services like physical therapy or nursing care, Medicare simply won't cover an aide for personal care alone.

To make this crystal clear, here’s a quick summary of what you need to know.

Medicare Home Health Aide Coverage at a Glance

This table breaks down the essentials of what Medicare requires versus what many people expect.

| Coverage Aspect | What This Means for You |

|---|---|

| Primary Need | You must first need skilled care (like nursing or physical therapy). The aide is a secondary, supportive service. |

| Duration of Care | Coverage is only for part-time or "intermittent" help. It will not cover 24/7 or long-term custodial care. |

| Type of Tasks | The aide helps with personal care (bathing, dressing) directly tied to your health condition, not homemaker tasks (cleaning, meals). |

| Doctor's Orders | A doctor has to create and regularly review a formal plan of care that certifies these services are medically necessary. |

Getting a handle on these fundamental rules is the first step. If your situation seems to line up with these initial criteria, the next step is to dig into the detailed eligibility requirements.

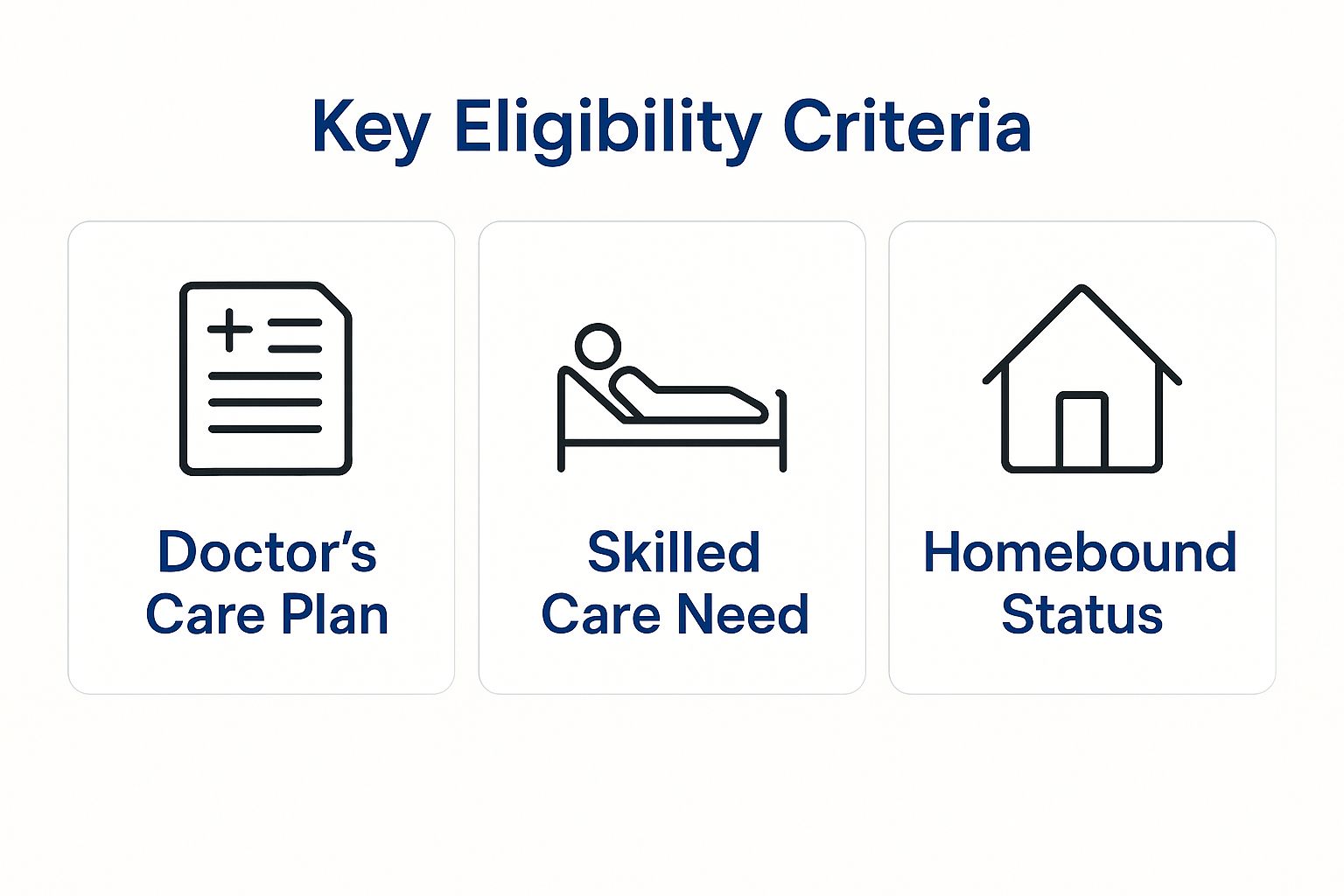

Meeting Medicare's Strict Eligibility Rules

Getting Medicare to pay for a home health aide isn't a given; it's a process with several strict checkpoints you have to pass. Think of it as a three-part key that unlocks the benefit. If you're missing even one piece, the door to coverage simply won't open.

The whole thing really comes down to what your doctor says is medically necessary. Without a physician directly involved and certifying your need, Medicare won’t even look at your request for home health services.

The Doctor's Critical Role

First things first, you have to be under a doctor's active care. It's this doctor who creates the formal plan of care, which is basically the official game plan for all your home health services.

This isn't just a casual note from your doctor. They must certify that the care is medically necessary for your condition, spell out exactly what services you need, and then regularly review that plan to make sure it’s still right for you as you recover.

The Need for Skilled Medical Care

The second big rule—and this is where a lot of people get tripped up—is that you must need skilled care on a part-time or intermittent basis. This is probably the most common point of confusion and the reason many requests end up getting denied.

Skilled care isn't just general help around the house. It refers to services that can only be done safely and correctly by a licensed professional. We're talking about things like:

- Skilled Nursing Care: This could be wound care, giving injections, or keeping a close eye on a serious health condition.

- Physical Therapy (PT): To help you get your strength and movement back after something like an injury or surgery.

- Occupational Therapy (OT): To help you relearn how to handle daily activities on your own.

- Speech-Language Pathology Services: To work on any issues with communication or swallowing.

A home health aide is only covered if you're also getting one of these skilled services. You can't qualify for an aide if all you need is personal care, like help with bathing or getting dressed. You can dig deeper into the specifics of the full Medicare home health benefits and see how all the pieces fit together.

Understanding the Homebound Requirement

The third and final piece of the puzzle is that your doctor must certify you as homebound. That word, "homebound," can sound a little scary, but it doesn't mean you're a prisoner in your own house.

Being "homebound" means that because of your illness or injury, leaving your home takes a considerable and taxing effort. Your doctor has to confirm that you either need help from another person or a device like a wheelchair or walker to get out, or that your condition makes leaving home medically inadvisable.

This infographic breaks down the three core eligibility requirements so you can see them side-by-side.

As you can see, all three parts—the doctor's plan, the need for skilled care, and being homebound—are equally vital. You have to meet all of them.

You can still be considered homebound if you leave for medical appointments, religious services, or to attend an adult day care center. Even an occasional short trip, like going for a haircut, is usually fine as long as it doesn't happen often. The main idea is that leaving home isn't a regular, easy thing for you to do.

What a Home Health Aide Is (and Isn't) Allowed to Do

So, you’ve navigated the Medicare eligibility rules and have been approved for home health care. Great! But now comes a crucial part: understanding exactly what a home health aide can and cannot do. This is where many families get tripped up, often expecting a housekeeper or personal chef, which can lead to a lot of frustration.

The key is to remember the aide’s role is laser-focused on supporting your medical recovery. They are there to help with the hands-on personal care you need because of your illness or injury—tasks you’d normally handle yourself but can’t right now.

Personal Care vs. Custodial Tasks

Medicare draws a very bright line between what it covers and what it doesn’t. It will pay for an aide to help with personal care, but it absolutely will not cover "custodial" or "homemaker" services if that's the only kind of help you need.

Getting this distinction right is fundamental. For a broader look at how these roles play out, it's helpful to understand the differences between home health and home care services.

The single most important takeaway is this: An aide's services are covered only when they are part of a broader, doctor-ordered plan that includes skilled nursing or therapy. Their job is to keep you safe and hygienic during your recovery, not to manage your household.

To make this crystal clear, let's break down the tasks side-by-side.

Covered Personal Care vs. Non-Covered Custodial Tasks

This table shows the specific types of "hands-on" personal care an aide can provide versus the household-related tasks that fall outside Medicare's coverage.

| Covered Personal Care Services | Non-Covered Homemaker/Custodial Services |

|---|---|

| Bathing and showering | General housekeeping and cleaning |

| Getting dressed and undressed | Cooking meals or meal delivery |

| Using the toilet and bathroom assistance | Shopping for groceries or running errands |

| Help with getting in and out of bed | Providing companionship or supervision |

As you can see, Medicare will cover an aide to help you bathe safely after a hip replacement, but it won't pay for someone to do your laundry or drive you to a doctor's appointment. The focus is squarely on personal hygiene and mobility support related to your medical condition.

Understanding the "Part-Time or Intermittent" Rule

Another critical limit you need to know about is the frequency of care. Medicare only covers home health aide services on a part-time or intermittent basis. This isn't just a suggestion; it's a hard rule that prevents families from using this benefit for full-time, round-the-clock support.

So, what does "intermittent" actually mean in the real world?

- It means care is provided for less than 8 hours per day.

- The total weekly hours are usually capped at 28 hours per week, though in some rare exceptions, this can go up to 35 hours.

This rule reinforces the entire purpose of the benefit: it’s for short-term, medically necessary help during a recovery period, not for ongoing, long-term daily care.

The Reality: Getting Home Health Aide Services Approved

Meeting Medicare’s eligibility criteria on paper is a great first step, but it doesn't guarantee you'll get the level of home health aide support your family might be expecting. It’s a tough but important truth: there’s often a huge gap between what the Medicare benefit technically allows and the actual services a home health agency will provide.

Even when your doctor certifies you need an aide, you might be surprised by how few hours or visits you’re actually offered. This isn't a mistake you made in the process. More often than not, it’s a reflection of bigger issues happening within the home healthcare industry itself.

Why Is There Such a Disconnect?

The root of the problem often comes down to how home health agencies get paid by Medicare. The current payment structure unintentionally creates a financial incentive for agencies to prioritize skilled nursing and therapy visits, which are reimbursed at a higher rate.

While an aide’s help with bathing and moving safely is absolutely vital for a patient, those personal care services are simply less profitable for an agency to provide. This creates a frustrating reality for families who need that hands-on help. You can be approved for care, only to find the agency can only send someone for a couple of hours a week, leaving you to fill in the rest.

This isn't a new problem. The data shows a sharp, years-long decline in the exact services families need most, making it hard to know if Medicare will pay for a home health aide in a truly meaningful way.

Ever since the payment system for home health was updated back in 2000, the use of aide services has plummeted. Research has found that home health aide visits dropped from about 2.2 visits per 30-day period in the late 1990s to just 0.5 visits in 2023. This happened even though Medicare's payments to agencies have been high enough to cover the cost. You can read the full research about these home health trends to get the bigger picture.

What This Means for Your Family

The main takeaway here is to be prepared. While Medicare’s home health aide benefit is a critical part of recovery for many people, it is almost never a complete solution for someone with ongoing personal care needs.

Think of Medicare-covered aide services as just one piece of a larger care puzzle, not the whole thing. The system is built to provide targeted, short-term support, and the industry's economic realities often squeeze that support even further. You will almost certainly need to look into other resources to supplement the hours Medicare will cover.

How Costs Differ Between Medicare Plans

So, will Medicare pay for a home health aide? One of the biggest questions on everyone's mind is what this will actually cost. The answer really boils down to which type of Medicare plan you have. Your out-of-pocket expenses can look very different if you're on Original Medicare versus a Medicare Advantage plan.

For folks with Original Medicare (that’s Part A and Part B), the financial side is refreshingly straightforward. If you check all the eligibility boxes, you’ll typically pay $0 for home health care services. That’s right—no deductible and no coinsurance for the aide, nursing visits, or therapy.

The only cost you might see is for medical equipment. You’ll pay 20% of the Medicare-approved amount for any durable medical equipment (DME), like a walker or hospital bed, that your doctor orders as part of your care plan.

Medicare Advantage Plan Costs

Now, if you have a Medicare Advantage (MA) Plan, sometimes called Part C, the rules of the game change a bit. These plans are run by private insurance companies that Medicare approves. While they are required by law to cover everything Original Medicare does, they can set their own rules for costs and how you access care.

This means that while your MA plan will definitely cover home health aide services, you might run into:

- Copayments or Coinsurance: You could have a flat fee for each visit or be on the hook for a percentage of the total cost.

- In-Network Requirements: Most MA plans have a network of approved providers. To get the best coverage, you'll need to use a home health agency that's in their network.

- Prior Authorization: It's very likely you'll need to get the insurance company's official green light before your home health services can start.

Does the Plan Type Really Change Who Gets Care?

Interestingly, even with these different cost structures, the number of people using home health services is almost identical between the two types of plans. This tells us something important: getting care isn't really driven by which plan you have, but by a clear, pressing medical need—like recovering from a hospital stay.

Data shows that the real trigger for home health care isn't the fine print in an insurance plan, but a significant medical event. The need for professional support after being in the hospital is what truly opens the door to these services.

For example, looking at 2025 data, home health care usage was nearly the same for both groups, with 8.4% of MA enrollees and 8.6% of Traditional Medicare beneficiaries getting this type of care. But after a hospital discharge? The numbers skyrocket to 41.5% for MA enrollees, proving the strong link between medical necessity and getting care approved, no matter the plan.

You can discover more insights about these Medicare home health trends to see just how much a medical event dictates the need for care.

What to Do When Medicare Coverage Is Not Enough

It’s a common and often stressful moment for families: the realization that Medicare’s home health aide benefit is a short-term, medical solution—not a long-term plan for daily living assistance.

When the covered hours run out, or your loved one needs non-medical custodial care, you’re left wondering what to do next. Fortunately, you have options. Understanding them is the key to building a sustainable care plan that truly works for your family.

Exploring Your Alternatives

Once Medicare’s coverage ends, the financial responsibility often shifts to the family. This is where long-term care planning becomes absolutely essential. Your primary alternatives include Medicaid, veterans’ benefits, and private payment arrangements.

-

Medicaid: Unlike Medicare, Medicaid is specifically designed to cover long-term care costs for people with limited income and assets. Many states have Home and Community-Based Services (HCBS) waiver programs that fund in-home care, helping individuals avoid moving into a nursing home.

-

Veterans Benefits: If your loved one is an eligible veteran or a surviving spouse, they may qualify for the VA Aid and Attendance benefit. This is a monthly pension supplement that can be used to pay for in-home care, including help with daily activities like bathing and dressing.

-

Long-Term Care Insurance: If you have a long-term care insurance policy, now is the perfect time to pull it out and review the details. These policies are built to cover the exact kind of custodial care services that Medicare doesn’t.

-

Private Pay: Many families ultimately pay for care out of their own pockets. While patient satisfaction with home health care is incredibly high at 91%, the costs can add up quickly. The median hourly rate for an aide is around $30, which can total $6,483 per month. This high cost highlights why it's so critical to explore every other funding source first.

Navigating these options requires careful planning and a clear understanding of the eligibility rules for each program. For a more detailed walkthrough, check out our complete guide on hiring a home health aide.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following all your specified requirements.

Your Top Questions About Medicare and Home Health Aides, Answered

Even when you think you have the rules down, real-life situations always bring up more questions. Let's walk through some of the most common things families ask when trying to figure out if Medicare will cover a home health aide.

Can I Get an Aide Just to Help with Bathing?

This is probably the number one question we hear, and the short answer is no. Medicare won't pay for a home health aide if personal care—like help with bathing, dressing, or meals—is the only thing you need.

Aide services are only covered when they support a broader plan of care that already includes skilled nursing or therapy.

Think of it this way: the need for skilled medical care is the key that unlocks the door. Without that key, Medicare sees personal care as "custodial," and that's simply not a covered benefit on its own.

How Do I Find an Agency That Accepts Medicare?

This part is critical. You absolutely have to use a home health agency that is officially certified by Medicare.

The easiest way to find a certified provider in your area is by using Medicare's own "Care Compare" tool right on their website. Your doctor's office or the discharge planner at the hospital are also great resources and can give you a list of local agencies they trust.

What if They Deny My Care or Try to Stop it Too Soon?

It's a scary thought, but you have rights. If your home health services are denied, cut back, or stopped before you feel you’re ready, you have the right to a formal appeal.

The agency is required to give you a written notice that explains their decision. That same notice will have clear instructions and deadlines for filing an appeal, which lets an independent third party review your case.

Trying to sort through all these care options can feel like a maze, but you don't have to find your way alone. If you need reliable, compassionate support at home, NJ Caregiving is here to help build a plan that truly fits your family. Find out more about how we can help.