When you first hear about "Medicaid payback," it's easy to picture the state swooping in to take a family home. The official term is Medicaid Estate Recovery, and while it sounds intimidating, it’s much more like a loan that only comes due after a person has passed away. The whole point is to help Medicaid continue serving those who need it most.

Demystifying Medicaid Estate Recovery

Let's clear the air. For many New Jersey families, the idea of Medicaid payback is a major source of stress. But the reality is a structured, federally mandated program with clear rules and limits. It’s not a free-for-all.

At its heart, this program is designed to recoup taxpayer money spent on specific long-term care services. Congress established the program back in 1993, requiring every state, including New Jersey, to have a system for recovering costs paid for long-term care. While the details can differ from state to state, the core idea is the same everywhere.

Who Is Affected by Payback Rules?

First off, estate recovery doesn't apply to every single person on Medicaid. The program specifically targets individuals who received certain types of long-term care services, typically those who were:

- Aged 55 or older when they received Medicaid benefits for things like nursing home care.

- Recipients of long-term care services, whether in a nursing home, an assisted living facility, or through extensive in-home care programs. You can get a better sense of what qualifies as long-term care in our detailed guide: https://njcaregiving.com/medicaid-long-term-care/

It's crucial to remember that the state cannot seek repayment while the Medicaid recipient is still alive. There are also significant protections for surviving family members. For example, the state has to wait if there's a surviving spouse, a child under 21, or a blind or disabled child of any age. This is a key safeguard designed to prevent vulnerable family members from being displaced.

To give you a sense of the scale, Medicaid programs across the U.S. collected about $733.4 million from estates in fiscal year 2019 alone. This shows just how integral it is to keeping the system funded.

So, what costs are we talking about? The state can generally recover expenses for nursing facility services, home and community-based services, and any related hospital stays or prescription drug costs. Once you understand these basics, you can start to see Medicaid payback not as a terrifying threat, but as a manageable part of long-term care planning. You can dig into these national collection statistics to see how they affect state-level programs.

To make things even clearer, here’s a quick breakdown of the core concepts.

Medicaid Payback At a Glance

This table simplifies the key ideas behind Medicaid Estate Recovery so you can grasp them quickly.

| Concept | Simple Explanation |

|---|---|

| What is it? | A federal requirement for states to recover the costs of long-term care from a deceased Medicaid recipient's estate. |

| Who is affected? | Primarily individuals aged 55+ who received long-term care services paid for by Medicaid. |

| What is an "estate"? | The property (like a house, car, or bank account) that a person owns at the time of their death. |

| Are there protections? | Yes. Recovery is delayed if there is a surviving spouse, a child under 21, or a blind or disabled child. |

Think of this as a quick-reference guide. The rules have nuances, but these are the foundational pillars of the program.

How the Estate Recovery Process Unfolds

When a loved one who received Medicaid passes away, their family is often left navigating a mix of grief and confusion. What happens now? The Medicaid estate recovery process isn't instant or arbitrary; it follows a clear, legally defined sequence.

Understanding this timeline can help remove a lot of the anxiety during an already difficult time. The journey begins the moment the individual passes, which sets in motion specific legal duties for the person handling their final affairs.

The Initial Notification and Claim Filing

The very first step is notifying the state. In New Jersey, the executor or administrator of the deceased person's estate is legally required to inform the state’s Medicaid agency of their passing. This notification is what officially starts the clock on the recovery process. A comprehensive settling an estate checklist can be an invaluable resource for navigating all the responsibilities that come up after a death.

Once notified, the agency gets to work. They calculate the total amount of benefits paid for the individual's long-term care services after they turned 55. Then, the agency formally files a claim against the estate for that amount, acting just like any other creditor would. This claim is a legal document that stakes the state's right to be paid back from the deceased's assets.

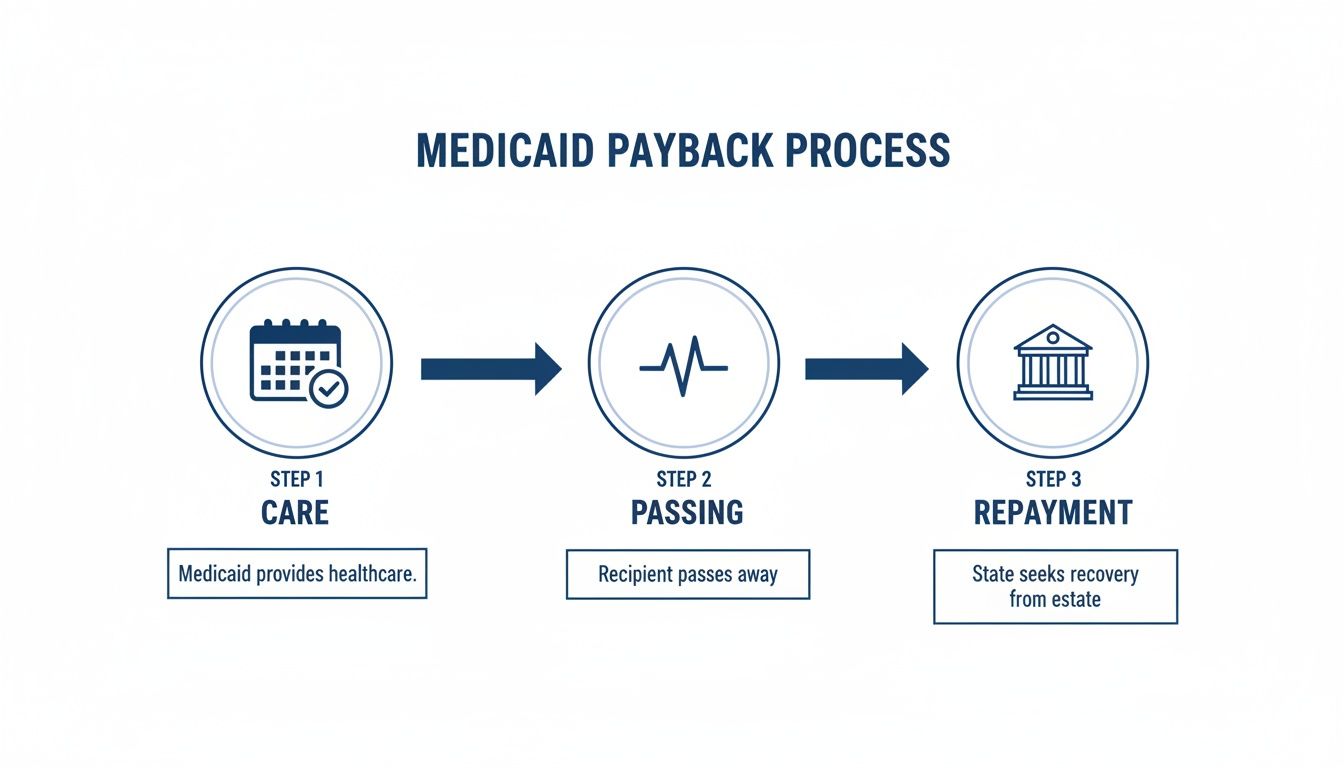

This infographic simplifies the flow of the Medicaid payback process.

As the visual makes clear, recovery is the final chapter, only beginning after the recipient’s death and based on the care they received.

Settling the Claim from Estate Assets

After the claim is filed, the estate’s representative has to deal with it as part of the probate process. Probate is simply the court-supervised procedure for validating a will, taking stock of assets, paying off debts, and distributing what’s left to the heirs.

The Medicaid claim has a specific place in the pecking order of debts. It typically gets paid after funeral expenses, the costs of administering the estate, and a few other high-priority creditors. But it must be paid before any money or property can be handed over to the beneficiaries named in the will.

A critical part of Medicaid payback rules is that the state can only recover up to the value of the assets in the estate. If the Medicaid bill is higher than what the estate is worth, the state can't come after the heirs personally for the difference.

Here’s the order of operations the executor must follow:

- Asset Collection: First, the executor gathers all the estate's assets—bank accounts, real estate, personal property, and anything else of value.

- Debt Payment: Next, they use the estate's funds to pay off all legitimate debts, including the Medicaid claim.

- Distribution to Heirs: Only when all creditors have been paid can the remaining assets finally be passed on to the heirs.

If the estate doesn’t have enough cash on hand to cover the claim, assets like the family home may need to be sold to satisfy the debt, unless a specific exemption applies. This is exactly why proactive estate planning is so crucial for families who want to protect their legacy.

Identifying Assets at Risk of Recovery

To really get a handle on Medicaid payback rules, you have to first understand what the state considers an "estate." This is where many families get tripped up. They assume it only covers assets that go through probate—the formal court process of distributing property after someone passes away.

But in New Jersey, the state takes a much, much broader view.

Think of the probate estate as just the starting point. This includes property titled only in the deceased person's name, with no beneficiary listed. These are the most obvious targets for recovery, but the state’s reach often extends far beyond them.

The Scope of New Jersey’s Expanded Definition

New Jersey law gives Medicaid the power to go after certain non-probate assets, too. These are assets that normally pass directly to a co-owner or a beneficiary without ever seeing the inside of a courtroom. Under specific circumstances, though, they can still be pulled back into the estate for recovery purposes.

This expanded definition is a critical piece of the Medicaid payback rules puzzle.

Here are some common assets that fall under this wider net:

- Jointly Owned Real Estate: A home owned as "joint tenants with right of survivorship" isn't automatically safe. The state can still place a claim against the deceased's share of the property's value.

- Assets in a Revocable Living Trust: Any property held in this kind of trust is almost always considered part of the estate when it comes to Medicaid recovery.

- Life Estates: If the Medicaid recipient kept a life estate interest in a property, the value of that interest can be targeted for repayment.

What this means is that simple strategies, like adding a child’s name to a bank account or the deed to the house, often don't provide the protection families think they do.

At the end of the day, the state’s goal is to get back the money it spent on care. So, any property interest the person held when they died—whether it goes through probate or not—is potentially on the table.

What Assets Are Commonly at Risk

Let's look at some real-world examples of property that frequently end up in the crosshairs of a Medicaid estate recovery claim in New Jersey. Seeing these specific examples helps families understand just how tangible the risk is.

Commonly Targeted Assets:

- The Family Home: This is the big one, both financially and emotionally. If it isn't protected correctly, it may have to be sold to pay back the state.

- Bank Accounts: Savings accounts, checking accounts, and money market funds that were solely in the deceased’s name are prime targets.

- Vehicles and Personal Property: Cars, boats, and other valuables are part of the probate estate and are fair game for recovery.

- Stocks, Bonds, and Investments: Any brokerage or investment accounts that don't have a designated beneficiary are included in the estate.

Just how aggressive a state is with recovery can vary a lot. While federal law sets the minimum requirements, many states go further. For example, 28 states will try to recover costs from some people under the age of 55, and 32 states seek repayment for all Medicaid benefits for those 55 and older, not just long-term care.

This is why understanding your state's specific rules is so crucial. You can discover more insights about these state-level variations on KFF.org to get a fuller picture of the potential risks.

When you first hear about Medicaid estate recovery, it’s easy to feel a little panicked. But the system isn't without a heart. Federal and New Jersey state laws have built-in safeguards to protect a family's most significant assets—especially the home—from a payback claim.

These exemptions aren't secret loopholes. They are intentional protections designed to prevent surviving family members from facing even greater hardship after a loved one passes away. Think of them as a legal shield. For many families, just knowing these exist is the first step toward peace of mind.

Exemptions That Protect Your Family's Assets

Absolute Protections for Surviving Family

Some situations put an immediate and indefinite stop to any estate recovery efforts. The state simply has to wait. These protections are all about keeping the immediate family stable and secure.

Recovery is automatically put on hold as long as the person who received Medicaid is survived by:

- A Spouse: The state cannot touch the estate as long as the deceased's spouse is alive. It doesn’t matter where they live. This crucial protection ensures the surviving spouse isn’t left without resources or a place to live.

- A Child Under 21: If there's a child under the age of 21, any recovery action is delayed until that child becomes an adult.

- A Blind or Disabled Child of Any Age: If the person who passed away has a child of any age who is blind or has a disability (as defined by Social Security), recovery is also postponed. This acknowledges that the child may depend on the estate's assets for their own care and housing.

These aren't just temporary fixes; they are firm legal barriers. The state can't move forward with its claim until the protected individual no longer meets the criteria—for instance, when the surviving spouse passes away or the minor child turns 21.

The table below breaks down who is protected and why, giving a clearer picture of these important safeguards.

Who Is Protected from Medicaid Estate Recovery

| Protected Individual | Condition for Exemption | Impact on Recovery |

|---|---|---|

| Surviving Spouse | Must be alive at the time of the recipient's death. | The state cannot pursue recovery as long as the spouse lives. |

| Minor Child | Must be under the age of 21. | Recovery is delayed until the child reaches the age of 21. |

| Blind or Disabled Child | Must meet the Social Security Administration's definition of blindness or disability. | Recovery is delayed indefinitely as long as the child remains disabled. |

These absolute protections provide a critical safety net, ensuring that the state's claim doesn't create a new crisis for the most vulnerable family members left behind.

The Caregiver Child Exemption

One of the most powerful and often-missed protections is the Caregiver Child Exemption. This incredible rule can protect the family home completely, allowing it to be transferred to an adult child without triggering a Medicaid penalty and shielding it from estate recovery later on.

It’s not for everyone, though. The adult child has to meet some very specific criteria:

- They must have lived in the parent's home for at least two full years right before the parent moved into a nursing facility.

- During those two years, they must have provided a level of care that kept the parent out of a nursing home.

This exemption is a powerful acknowledgment of the immense value that family caregivers provide. By keeping a loved one at home, they save the Medicaid system significant expense, and this rule allows them to inherit the home in return.

Let's make this real. Imagine a daughter moves in with her aging father. For three years, she helps him with meals, medications, and getting around. Her care allows him to stay in his beloved home far longer than he otherwise could have. When he eventually does need to move to a nursing home, this exemption could allow him to transfer the house to her, protecting it from a future payback claim.

For families in this situation, it's essential to explore all your options for protecting assets from nursing home costs with an experienced professional.

The Undue Hardship Waiver

So, what happens if none of those absolute protections apply, but losing the family home would cause a genuine financial disaster for an heir? This is where the undue hardship waiver comes into play.

Heirs can formally ask the state to waive its recovery claim if they can prove it would create an "undue hardship." Each state defines this a little differently, but it generally applies if the heir:

- Has a low income and the home is their only place to live.

- Would be forced to go on public assistance if the state seized the asset.

- Was financially or medically dependent on the person who passed away.

Requesting this waiver involves a formal application with detailed financial proof sent to the state Medicaid agency. It’s definitely a last line of defense, but it provides a critical safety net for heirs who would otherwise be left completely destitute by the estate recovery process.

Proactive Strategies to Safeguard Your Assets

While understanding exemptions is a good first step, the best defense against Medicaid payback rules is a good offense—planning years ahead. By taking proactive measures, you can legally and ethically structure your assets to protect them from future estate recovery claims. This isn't about hiding money. It’s about using established legal tools to preserve your family's financial security.

The absolute cornerstone of this kind of planning is the five-year look-back period. This rule exists to stop people from giving away all their assets right before they apply for Medicaid. Any gifts or transfers made for less than what they're worth within five years of applying can trigger a penalty period, making the applicant ineligible for benefits.

This means any serious asset protection strategy has to start long before a health crisis hits. Waiting until you need long-term care is almost always too late. For families who want to dig deeper into these tactics, this guide on how to avoid Medicaid estate recovery offers some great state-specific insights.

The Power of an Irrevocable Trust

One of the most effective tools an elder law attorney has is the Irrevocable Trust. Think of it like a secure lockbox where you place valuable assets, such as your home. Once something is inside an irrevocable trust, you no longer legally own it—the trust does.

That's a critical difference. Because the asset is no longer part of your personal estate, it's generally safe from Medicaid estate recovery. For this to work, the trust has to be set up—and the assets transferred into it—more than five years before you apply for Medicaid. This is how you stay on the right side of the look-back rule.

An irrevocable trust legally separates your most valuable assets from your name, placing them outside the reach of Medicaid estate recovery. This strategy requires careful planning with a legal professional but offers one of the strongest forms of protection available.

Setting one up is a major legal decision. "Irrevocable" means exactly what it sounds like: you can't just change your mind and pull the assets back out. But for anyone serious about long-term planning, it provides unmatched peace of mind.

Strategic Asset Transfers and Gifts

Another common strategy is gifting or transferring assets directly to family members. This sounds straightforward, but it has to be handled with extreme care because of that five-year look-back period. For example, a parent could transfer the deed of their home to their children.

If that transfer happens six years before the parent applies for Medicaid, the house is typically safe from both eligibility penalties and estate recovery. But if it happens inside that five-year window, it will almost certainly cause a long period of ineligibility. You can learn more about how asset limits come into play in our guide to New Jersey's Medicaid spend-down rules.

This approach has its own set of risks, though. The moment you transfer an asset, you give up control. The new owner could get divorced, run into creditor problems, or decide to sell it—all of which could put the asset you were trying to protect at risk.

Considering Long-Term Care Insurance

Long-term care (LTC) insurance is another key piece of a proactive plan. It's not a direct way to avoid Medicaid recovery, but it can help you avoid needing Medicaid in the first place.

Here’s how it fits into the puzzle:

- Pays for Care: LTC insurance is designed specifically to cover the staggering costs of nursing homes, assisted living, or in-home care.

- Preserves Assets: By using insurance benefits to pay for care, you don't have to drain your life savings to become eligible for Medicaid.

- Avoids Recovery: If you never have to apply for long-term care through Medicaid, the Medicaid payback rules simply don't apply to your estate.

When you combine LTC insurance with legal tools like an irrevocable trust, you create a powerful, multi-layered defense. The insurance provides the money for care, while the trust protects your core assets, making sure they can be passed down to the next generation.

Responding to a Medicaid Claim After a Death

Receiving a formal notice from the state while you're grieving a loved one can feel like a punch to the gut. It’s jarring and overwhelming. But when New Jersey’s Medicaid agency sends a claim, it's a legal document that requires a steady, methodical response—not panic.

Your first instinct might be to set it aside, but it’s crucial to avoid ignoring the notice. The claim isn’t going away. In fact, delaying your response will only complicate the process of settling the estate. Think of it as one of the essential administrative tasks that needs to be handled.

Your Initial Action Plan

The best way to navigate this is to get organized and seek professional advice right away. The person in charge of handling the estate—the executor or administrator—should take the lead on this.

Here’s a simple checklist to get you started:

- Gather Key Documents: Round up all the important paperwork. This includes the deceased's will, the death certificate, and any documents related to their assets, like home deeds and bank statements. You'll also need the official claim notice from Medicaid.

- Do Not Distribute Assets: This one is critical. Hold off on paying heirs or giving away any property from the estate until the Medicaid claim and all other debts are fully resolved. If you distribute assets too soon, the executor could be held personally liable.

- Consult an Elder Law Attorney: This is, without a doubt, the most important step you can take. An attorney who specializes in this area can review the claim for accuracy, figure out if any exemptions apply, and respond to the state on your behalf.

An experienced attorney is your best advocate. They can comb through the state’s accounting for any errors and explore powerful options like the undue hardship waiver, which can protect heirs from what might otherwise be a devastating financial loss.

Understanding Your Rights and Responsibilities

It's important to know that the estate is responsible for paying the claim, not the individual heirs. The state can only recover money up to the value of the assets in the estate.

For example, if the claim is for $80,000, but the estate is only worth $50,000, the state receives the $50,000. The remaining $30,000 of debt is effectively forgiven. Heirs are never required to pay the difference out of their own pockets.

Properly responding to the claim notice is a vital part of honoring your loved one’s final affairs. By following these steps and getting the right guidance, you can manage this responsibility with confidence and bring things to a proper close.

Common Questions About NJ Medicaid Payback Rules

Trying to understand Medicaid estate recovery can feel overwhelming, and it often brings up very specific, personal questions. We've put together answers to some of the most common concerns we hear from New Jersey families to help you get the clarity you need to make the right decisions.

Does Medicaid Always Take Your House In New Jersey?

No, and this is probably the biggest myth out there. Medicaid can't touch your house as long as you, your spouse, or a dependent or disabled child of any age is living there. The state's ability to make a claim is put on hold until all of those protected individuals have either passed on or moved out.

Once that happens, the state can then look to recover costs from the value of the home, which usually means the house has to be sold. But here's the good news: with some smart, proactive planning—like setting up an irrevocable trust or transferring the home well before the five-year look-back window—you can often protect the house completely from a future claim.

How Does the 5-Year Look-Back Period Affect Payback Rules?

It's easy to get these two mixed up, but the five-year look-back and estate recovery are separate things that work together. The look-back period is all about Medicaid eligibility (getting approved), while estate recovery is what happens after death (settling the bill).

The look-back rule is designed to penalize people who gave away assets or sold them for cheap within five years of applying for Medicaid. This connects directly to payback because any steps you take to avoid estate recovery, like giving your house to your kids, must be done more than five years before you apply. If not, you’ll face a penalty period where you won't be eligible for benefits.

Think of it like this: The look-back period is the gatekeeper checking your bags before you get on the plane. The payback rule is the airline settling your final tab after the trip is over. You have to plan for both.

Can Medicaid Take My IRA or 401(k) After I Pass Away?

It's a definite possibility. While you're alive, retirement accounts like an IRA or 401(k) are usually considered "non-countable" assets for eligibility, as long as you're taking your required minimum distributions. This is great because it means you can qualify for care without having to liquidate your life savings.

The problem comes after you pass away. Any money left in those accounts that gets paid out to your estate becomes a probate asset. And once it’s part of the probate estate, it’s fair game for Medicaid to make a claim to repay the cost of your care.

The most effective way to sidestep this is to name a specific person (not "my estate") as the direct beneficiary on every single one of your retirement accounts. Doing this keeps the money out of the probate process and shields it from recovery.

Is It Possible to Challenge a Medicaid Estate Recovery Claim?

Yes, you absolutely have the right to challenge a claim from the state. Your family isn't powerless. There are a couple of main avenues for this:

- Undue Hardship Waiver: This is the most common path. You can apply for a waiver if you can prove that losing the asset would cause you significant financial distress. A classic example is if the asset is a modest home that is your primary residence and you have a very low income.

- Disputing the Amount: You can also fight the bill itself. If you suspect there are mistakes in how the state calculated the benefits paid, you can request an itemized accounting and challenge the total.

If you get a notice of a claim, the best first step is to speak with an experienced elder law attorney. They can spot any errors in the claim, help you determine if you qualify for a hardship waiver, and make sure your family’s rights are protected every step of the way.

At NJ Caregiving, we understand that planning for long-term care involves navigating complex rules and making difficult decisions. Our compassionate in-home care services are designed to help your loved ones live with dignity and independence in the comfort of their own homes. If you need support for a family member in Mercer County, visit us at https://njcaregiving.com to learn how we can help.