When you're trying to figure out the best way to care for a loved one, one of the biggest questions that comes up is money. How much does in-home senior care actually cost? It’s a huge factor in any family's decision-making process.

Across the country, the typical hourly rate for a professional caregiver lands somewhere between $25 and $35. Of course, that final number can shift quite a bit depending on where you live and the exact kind of support your family member needs.

What Is the Average Cost of In Home Senior Care

Getting a handle on the numbers behind in-home care is the first step toward building a plan that feels both confident and sustainable. It helps to think of hiring a caregiver like you would any other skilled professional, whether it's a plumber or an electrician. You’re paying for their time and expertise, but you're also paying for something invaluable: peace of mind.

The final cost isn't one-size-fits-all because every person's situation is unique. Someone who primarily needs a friendly face for companionship and a hand with errands will naturally have a different cost than someone who needs help with personal tasks like bathing or specialized support for a chronic illness.

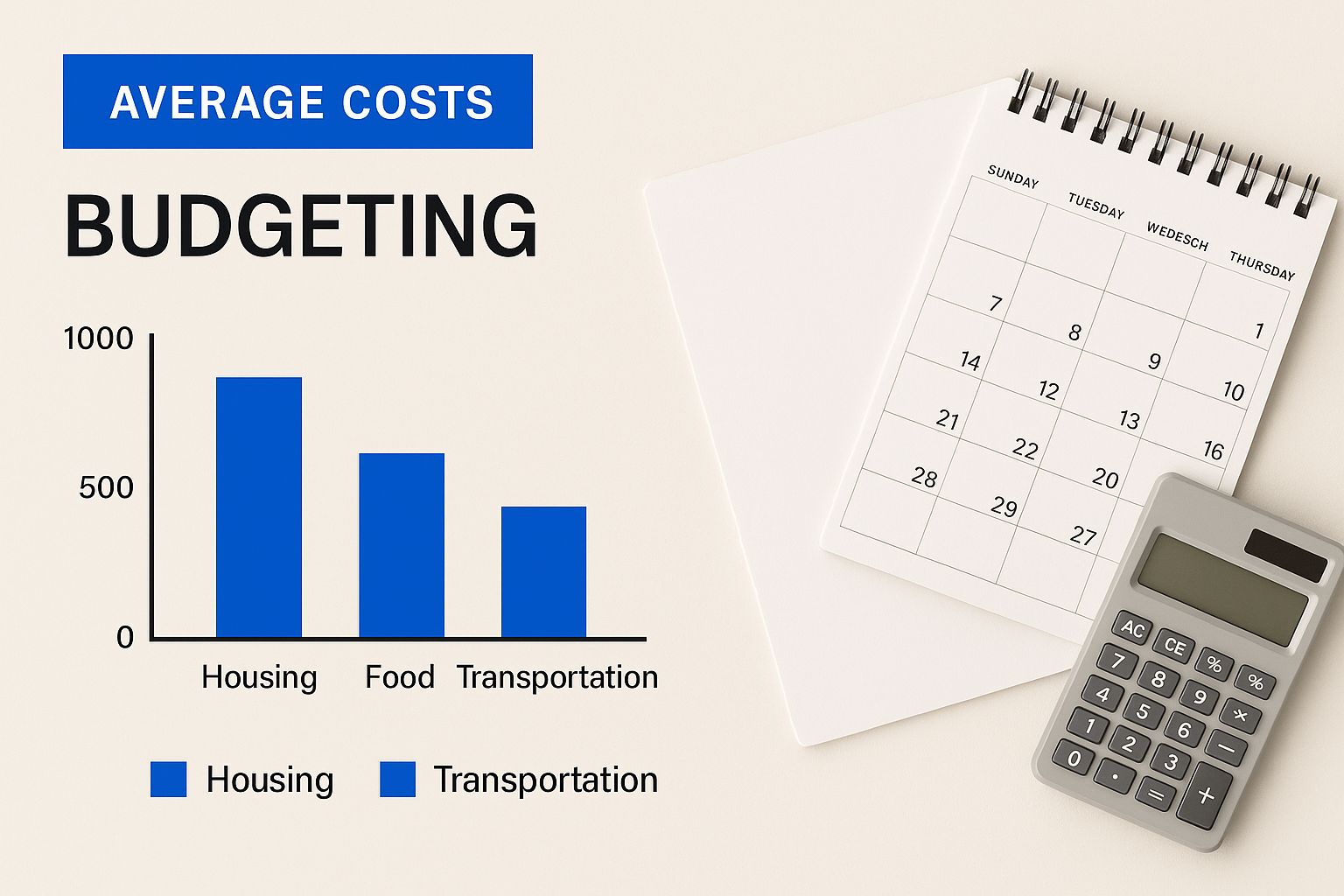

Breaking Down the Hourly Rates

The hourly rate is the foundation of your in-home care budget. Research from 2025 shows that the average cost for in-home senior care in the U.S. falls between $25 and $35 per hour. This range is pretty wide for a reason—it accounts for everything from the caregiver's qualifications and the complexity of the care to major differences in cost of living from one state to the next.

It's also common for agencies to offer better rates for longer shifts, so it pays to ask. You can find more great insights into these pricing factors by exploring in-home care costs in 2025.

To give you a better feel for what you’re getting, let's break down what those rates usually cover.

Key Takeaway: The hourly rate is the fundamental building block of your total in-home care budget. By understanding this number, you can better estimate weekly and monthly expenses.

A Quick Look at In-Home Senior Care Hourly Rates

Not all care is created equal, and the price often reflects the level of skill involved. For example, non-medical companion care is usually the most budget-friendly option. On the other hand, services that require a certified nursing assistant (CNA) or a registered nurse (RN) will be at the higher end of the scale.

The table below gives you a simple overview to help set your expectations.

| Care Service Type | Average Hourly Cost Range | Common Services Included |

|---|---|---|

| Companion Care | $25 – $30 | Companionship, light housekeeping, meal preparation, errands, and transportation. |

| Personal Care | $28 – $33 | All companion services plus hands-on help with bathing, dressing, grooming, and mobility. |

| Skilled Nursing Care | $35+ | Advanced medical tasks like wound care, medication administration, and monitoring vital signs. |

Think of this table as a starting point. Your best bet is always to get specific quotes from agencies in your area. The in home senior care cost in a major city will almost always be higher than in a rural town, simply because of differences in wages and the cost of living.

Once you have a grip on these initial numbers, you can start building a financial plan that truly works for your family.

Of course. Here is the rewritten section, crafted to sound like an experienced human expert and match the provided examples.

The Key Factors That Shape Your Final Care Cost

Knowing the national average for in-home care is a great starting point, but it's just that—a start. You might be wondering why one family pays $25 an hour while their neighbor pays closer to $35. The reality is, the final in home senior care cost is not a one-size-fits-all number. It’s a dynamic price shaped by a few very important variables.

Think of it like building a custom home. You have a base price to get the project started, but the final cost really depends on the floor plan, the materials you choose, and any special features you add. In-home care works the same way. Your family’s unique needs and circumstances are the blueprints that will determine the final bill. Getting a handle on these factors will help you anticipate expenses and have much more productive conversations with care providers.

The Type and Level of Care Needed

The biggest driver of your final cost is the type of care your loved one requires. Not all assistance is created equal, and the price tag directly reflects the caregiver's skill level and the complexity of their duties. Care services generally fall into a few main categories, each with a different price point.

For example, companion care is often the most affordable route. This service focuses on providing emotional support, helping with light housekeeping, and keeping your loved one socially engaged. If more hands-on help is needed, you're looking at personal care, which covers assistance with activities of daily living (ADLs) like bathing, dressing, and getting around safely. This requires more training for the caregiver, and the hourly rate reflects that.

The highest tier is skilled nursing care. This involves medical tasks that can only be performed by licensed professionals like Registered Nurses (RNs) or Licensed Practical Nurses (LPNs), such as wound care, administering injections, or managing complex medical equipment.

According to a study from the U.S. Department of Health and Human Services, men typically require long-term care for an average of 2.2 years, while women need it for about 3.7 years. This really underscores how important it is to budget for the right level of care over the long haul.

The Impact of Your Location

Where you live plays a massive role in what you’ll pay for care. Just like a gallon of milk costs more in a big city than in a small town, the price of in-home care can vary dramatically from one state—or even one city—to the next.

This regional price difference comes down to a few economic realities:

- Cost of Living: In areas with higher housing prices, groceries, and other expenses, caregiver wages naturally have to be higher.

- Local Demand: Big metropolitan areas with large senior populations often have more demand for caregivers, which can push prices up.

- State Regulations: Things like minimum wage laws and state-specific requirements for caregiver certification also factor into the hourly rates.

It's not uncommon for a family in a major urban center to pay 15-25% more for the exact same services than a family living in a more rural community.

Scheduling and Hours of Service

When and how often you need care are also key cost drivers. Standard daytime hours on weekdays will always be the most budget-friendly option. But as we all know, care needs don't always stick to a neat 9-to-5 schedule.

Here’s a quick look at how scheduling can affect your bill:

- Overnight Care: A caregiver who needs to be awake and alert all night will cost quite a bit more than one who is simply on-hand for emergencies and can sleep.

- Weekend and Holiday Care: You can definitely expect to pay a premium for services on weekends and major holidays. Caregivers are often paid time-and-a-half for working these hours.

- Part-Time vs. Full-Time: While the hourly rate might be a little lower if you book full-time (40+ hours per week) care, your total monthly cost will obviously be higher. On the flip side, very short shifts of just a couple of hours might come with a higher hourly rate to make the caregiver's travel and time worthwhile.

Understanding these variables is the key to building a realistic and sustainable budget. By taking a clear-eyed look at your loved one's specific needs, your location, and the schedule required, you can move from a ballpark estimate to a solid financial plan.

How In-Home Care Compares to Other Senior Living Options

Choosing the right care setting for a loved one is a delicate balancing act. It’s about more than just money—it’s about their happiness, independence, and well-being. As families start this journey, one question always comes up: is it actually more affordable for Mom or Dad to age in place at home than to move into a facility?

The answer isn't a simple yes or no. The cost of in-home senior care really depends on how much support is needed.

Think of it like planning a vacation. You could book your flight, hotel, and meals separately—à la carte style. If you just need the basics, this can be a very budget-friendly way to go. But once you start adding guided tours, fancy dinners, and daily activities, the costs can quickly climb and might even surpass an all-inclusive resort package. In the same way, part-time home care is often the most economical choice, but full-time, around-the-clock care can have a price tag similar to a residential facility.

This graphic gives you a quick visual of how those average costs stack up.

As you can see, while part-time home care has a clear cost advantage, the financial gap starts to shrink when you compare it to assisted living. Full-time nursing care, however, remains in a category of its own as the most expensive option.

A Head-to-Head Financial Comparison

To make a truly informed choice, you need to see the numbers side-by-side. For most families, the monthly bill is the biggest piece of the puzzle when creating a long-term care budget. When you break it all down, the financial landscape of senior care becomes much easier to navigate.

Recent data paints a pretty clear picture. In 2025, the average monthly cost for in-home personal care in the U.S. is about $5,417. If more medical support is needed from a home health aide, that number nudges up to $5,625. What's interesting is that assisted living facilities often land in a nearly identical range, from $5,417 to $5,625 per month. The big jump comes with nursing home care, where a semi-private room averages a steep $8,641 monthly, and a private room climbs even higher to $9,872. You can find a more detailed look into these senior care cost comparisons from Ultimate Care.

Here's a simplified look at how these options compare each month.

Monthly Senior Care Cost Comparison

| Care Option | Average Monthly Cost | Key Benefits |

|---|---|---|

| In-Home Care | $5,417 – $5,625 | Provides one-on-one attention and allows seniors to remain in the comfort and familiarity of their own home. |

| Assisted Living | $5,417 – $5,625 | Offers a community setting with built-in social activities and on-site support for daily living tasks. |

| Nursing Home | $8,641 – $9,872 | Delivers 24/7 medical supervision and skilled nursing care for individuals with complex health needs. |

This comparison really highlights a key takeaway: for many families, the cost of full-time home care and assisted living can be surprisingly close.

Beyond the Price Tag: The Value of One-on-One Care

While the finances are critical, the decision can't be based on numbers alone. The "value" you get from each option goes far beyond the monthly invoice. In-home care, in particular, offers profound benefits that are hard to put a price on but are incredibly important to a senior's quality of life.

Key Insight: The biggest advantage of in-home care is the dedicated, one-on-one attention a senior receives. In a facility, staff members have to divide their time and focus among many residents. At home, the caregiver’s only priority is your loved one’s needs, comfort, and safety.

This personalized approach creates several invaluable outcomes:

- Greater Independence: Seniors get to keep their own routines, live by their own rules, and stay surrounded by familiar furniture, photos, and memories.

- Enhanced Comfort and Dignity: Being in a familiar, comfortable environment naturally reduces stress and anxiety, promoting a much stronger sense of security and personal dignity.

- Customized Support: Care plans are built around the person, not the facility's schedule. This ensures that help is there exactly when and how it's needed.

Ultimately, weighing the cost of in-home care against other options means looking at the whole picture. You have to consider both the financial investment and the profound emotional and psychological benefits of allowing a loved one to age with dignity in the place they truly call home.

Decoding the Price of 24-Hour In-Home Care

The idea of having a dedicated professional available around the clock gives families incredible peace of mind, but let's be honest—the potential price tag can feel intimidating. When a loved one needs constant supervision, the conversation about in-home senior care cost quickly moves past hourly rates and into what a comprehensive, 24/7 plan looks like. Breaking down how this intensive level of support is priced is the first step toward making a sustainable decision.

First, it’s important to understand what "24-hour care" actually involves. This isn't one person working themselves to the bone. For safety, quality, and legal reasons, round-the-clock care is delivered by a team of caregivers working in shifts. This usually means two 12-hour shifts or three 8-hour shifts to ensure a fresh, alert professional is always on hand. This is a very different setup from "live-in care," where a single caregiver lives in the home and has designated time off for sleep and personal breaks.

Why 24-Hour Care Carries a Premium Price

Because 24-hour care requires multiple caregivers to cover a full 168 hours a week, the cost is naturally much higher than standard part-time help. You're essentially covering the wages for two or three full-time positions. This continuous, active support is exactly what drives the premium price.

The numbers certainly reflect this high level of service. Looking at the cost of 24-hour in-home care in the U.S. for 2025, the median monthly expense is about $18,144. This figure can easily range from $15,000 to over $25,000 per month, depending on your location and the complexity of the care needed. In major cities with a higher cost of living, like Boston, hourly rates often hit the top of this scale, averaging around $27 per hour. Despite the significant investment, many families find the value of personalized attention in a familiar, comfortable setting is absolutely worth it. You can get a deeper dive into how 24/7 care costs are calculated.

Key Takeaway: The cost of 24-hour care isn’t just about having someone present; it’s about paying for continuous, active support from a dedicated team of professionals, which explains the substantial monthly expense.

When Is This Level of Care Truly Necessary?

While the security of 24/7 care sounds great, it’s not always the right or necessary choice for every family. It’s a solution best reserved for specific, high-need situations where safety is a primary and constant concern. By taking a hard look at your loved one's needs, you can figure out if this intensive support is the most appropriate and financially responsible path.

See if your loved one’s situation fits into one of these categories:

- Advanced Dementia or Alzheimer’s: For individuals who experience sundowning, wander, or have severe cognitive decline, constant supervision is crucial to prevent accidents or injury.

- Significant Fall Risk: When a senior has extreme mobility issues or a condition that makes them highly susceptible to falls, having a caregiver always present can be truly lifesaving.

- Post-Surgery or Complex Medical Recovery: After a major operation or hospital stay, someone might need continuous help with repositioning, medication reminders, and personal care to ensure a safe recovery at home.

- End-of-Life or Hospice Care: During the final stages of life, 24-hour care provides the patient and their family with essential medical support, comfort, and emotional reassurance when they need it most.

Making the call to bring in 24-hour care is a major step. It requires carefully weighing your loved one's needs against the significant financial commitment to ensure it’s a choice that promotes both well-being and long-term stability for everyone involved.

Finding Ways to Pay for In-Home Care

Figuring out the potential in-home senior care cost is a huge step, but what comes next is often the toughest question: where does the money come from? It’s easy to feel overwhelmed by the numbers, but there are more financial avenues available than you might think. You don’t have to figure this out on your own.

Think of it like putting together a financial toolkit. You probably won't use every single tool, but knowing what's in the box gives you options and a sense of control. From personal savings and insurance policies to government aid, you can often weave together a strategy that makes quality care sustainable. Let's walk through the most common ways to fund the care your loved one needs.

Private Pay and Long-Term Care Insurance

The most straightforward way to pay for care is through private funds—things like personal savings, retirement accounts (like a 401(k) or IRA), or annuities. A 2019 study found that about two-thirds of adults over 65 (who aren't on Medicaid) could cover at least two years of home care with their income and liquid assets. While that sounds good, it might not be enough, since women need care for an average of 3.7 years and men for 2.2 years.

This is where Long-Term Care (LTC) insurance can be a game-changer. These policies are specifically designed to cover the very services that regular health insurance won't, including the personal, non-medical care that happens in the home.

An LTC policy works simply: you pay premiums over time, and if you later need help with daily activities, the policy pays a benefit to cover those care costs. It can be a financial lifesaver, but you have to know the details:

- Elimination Periods: Think of this as a deductible measured in time, not dollars. It’s a waiting period (often 30-90 days) before the policy starts paying out.

- Benefit Caps: Most policies have a lifetime maximum payout. It’s critical to know what that limit is.

- Coverage Specifics: Policies aren't one-size-fits-all. You need to confirm that your specific policy covers non-medical in-home care, as some are more restrictive than others.

Understanding Medicare and Medicaid's Roles

Many families are shocked to learn that Medicare plays a very limited role in covering ongoing in-home care. It’s a common and costly misconception.

Medicare is built for short-term, skilled medical care after an injury or hospital stay. It does not typically pay for long-term "custodial" care—the help with personal tasks like bathing, dressing, and meals—unless you're also getting skilled care at the same time.

Medicaid, on the other hand, is a vital resource for families with limited income and assets. It's the largest public payer for long-term care services in the U.S.

Medicaid offers programs called Home and Community-Based Services (HCBS) waivers. These are designed specifically to help eligible seniors get care in their own homes instead of moving to an institution like a nursing home. In New Jersey, for instance, programs like Managed Long-Term Services and Supports (MLTSS) are a lifeline for thousands of qualifying residents.

Exploring Veterans Benefits and Other Avenues

Beyond the big insurance and government programs, other valuable resources can help lighten the load. It’s worth exploring every single option to build a solid financial plan.

One of the most significant—and often overlooked—resources is for those who served our country.

Veterans Affairs (VA) Benefits

The Department of Veterans Affairs offers programs that can provide serious financial help for in-home care. The best-known is the Aid and Attendance benefit, a monthly pension supplement for wartime veterans and their surviving spouses. If you meet the criteria, this benefit can be used to pay for help with daily living activities.

A few other options might also be on the table:

- Reverse Mortgages: For seniors who own their homes, a reverse mortgage lets them tap into their home equity for cash. It can provide a steady income stream for care, but it’s a major financial decision. Always discuss this with a trusted financial advisor.

- Local and State Programs: Your local Area Agency on Aging is a goldmine for finding smaller, state-specific programs that might offer grants or subsidized care. For families in Mercer County, organizations like NJ Caregiving are fantastic at connecting people with these local resources.

By mixing and matching these different funding streams, you can build a robust plan to manage the cost of in-home senior care without breaking the bank.

Creating a Sustainable In-Home Care Budget

Alright, let's turn those abstract numbers into a real, workable plan. Building a budget for in-home care is about more than just managing the in home senior care cost—it’s about creating a financial path that eases the stress for everyone involved. A well-planned budget gives you clarity and confidence during what can be a really challenging time.

Think of it like getting ready for a big road trip. You wouldn't just hop in the car and start driving. You’d map your route, figure out what gas will cost, and plan for stops along the way. Budgeting for care needs that same kind of thoughtful prep to make sure the journey is as smooth as possible. This simple framework will give you a clear roadmap to manage costs without the anxiety.

Step 1: Assess Your Loved One’s Exact Needs

Before you can even think about a budget, you need a crystal-clear picture of what support is actually needed. A thorough assessment is the foundation for your entire plan. Is the main thing they need companionship and some help with housekeeping, or are we talking about hands-on personal care like bathing and mobility support?

Make a detailed list of every single task, from cooking meals to reminding them about medications. This will help you figure out the skill level you need in a caregiver and, just as importantly, get a good estimate of how many hours of care per day or week are necessary. Getting this right from the start keeps you from over or underestimating what you truly need.

Step 2: Research and Account for All Costs

With your list of needs ready, you can start looking into local rates. But remember, the caregiver's hourly wage is just one part of the financial picture. You have to account for all the other potential expenses to avoid any nasty surprises down the road.

Be sure to factor in these often-overlooked costs:

- Agency Fees: If you go through an agency, their rates usually bundle in administrative costs, insurance, and the work they did screening caregivers.

- Supplies: This can be anything from gloves and incontinence products to specific foods for special dietary needs.

- Home Modifications: You might need to set aside money for small but important safety updates, like installing grab bars in the bathroom or getting a shower seat.

A study from the U.S. Department of Health and Human Services found that women, on average, need long-term care for 3.7 years, while men need it for 2.2 years. This really highlights why building a detailed, forward-thinking budget is so critical for long-term financial peace of mind.

Step 3: Have Honest Conversations with Family

Talking about money is rarely easy, but it's an absolutely vital part of this process. Once you have a realistic cost estimate, it's time to bring the family together to discuss how these expenses will be handled. Being open and transparent is your best strategy for avoiding misunderstandings and resentment later.

The goal here is to agree on a plan that everyone feels is fair and doable. This might mean pooling resources, splitting up different responsibilities, or looking into financial aid options together. These conversations get everyone on the same page, creating a united team to support your loved one. With a clear plan in place, you can all focus on what really matters: providing warm, compassionate care.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following all your specified requirements.

Common Questions About Home Care Costs

When you start digging into the finances of in-home care, you’re bound to have questions. It’s one thing to do the initial research, but it’s another to make real, concrete plans for your family. As you get closer to a decision, new concerns always seem to pop up.

Let's walk through some of the most common questions we hear from families, so you can feel more confident about handling the financial details.

Can We Deduct Home Care Costs on Our Taxes?

Yes, in many situations, you absolutely can. If the care allows you or your spouse to go to work, you might be able to claim the Child and Dependent Care Credit.

More often, families find they can deduct these costs as medical expenses. If your loved one is considered your dependent, you can potentially deduct their qualifying care expenses that exceed 7.5% of your adjusted gross income (AGI). The key here is that the care must be medically necessary and prescribed by a doctor, which often includes personal care services for someone managing a chronic illness.

This part of the tax code can get tricky, so we always recommend touching base with a tax professional. They can make sure you're getting every deduction you're entitled to while staying on the right side of IRS rules.

Key Insight: Don't let potential tax savings slip by. Keeping detailed, organized records of every care-related expense is your best friend come tax time. Just be sure you understand the specific IRS requirements for medical deductions.

How Do We Plan for Future Cost Increases?

It’s a fact of life: the cost of care doesn’t stay the same. Between inflation and rising wages for caregivers, you can expect prices to creep up over time. Building this reality into your budget from day one is the best way to create a plan that lasts.

As a general rule, it's wise to budget for a 3-5% increase in costs each year. Factoring this in from the get-go helps avoid sticker shock and financial stress down the road.

Here’s how you can stay ahead of the curve:

- Annual Budget Review: Make it a yearly ritual to sit down, look at the numbers, and adjust your financial plan.

- Look into Long-Term Care Insurance: Many policies offer inflation protection riders, which are designed to increase your daily benefit over time to keep up with rising costs.

- Keep an Emergency Fund: A separate savings account for unexpected care costs or sudden rate hikes can be a true lifesaver.

By getting answers to these common questions, you're in a much better position to create a solid, sustainable financial plan for your loved one's care.

At NJ Caregiving, we know that figuring out the financial side of care can feel overwhelming. Our mission is to provide compassionate, top-quality in-home care and help families in Mercer County understand all their options, including Medicaid. To learn how we can support your family, visit us at https://njcaregiving.com.