When you first start looking into home health care, you’ll likely see an average cost somewhere between $25 and $35 per hour. But it's important to treat that number as just a starting point. The final price tag is entirely personal, shaped by your specific needs, where you live, and the level of medical expertise required.

Understanding the True Cost of Care

The initial price can seem simple enough, but home health care is much more like a personalized service than a one-size-fits-all product. That hourly rate is the basic building block, but several other layers contribute to the final monthly or annual expense. Getting a handle on these components is the first step toward building a care plan that’s both effective and sustainable for you or your family.

Think of it like hiring a contractor for a home renovation. A simple paint job (similar to basic companionship) is going to cost a lot less than a full kitchen remodel that requires a licensed electrician and a master plumber (like skilled nursing care). Every project has a different scope, demands a unique set of skills, and naturally, comes with a different price.

Breaking Down the Hourly Rate

That national average is a useful benchmark to have in your back pocket. Looking ahead to 2025, the average cost for in-home care in the United States is projected to be between $25 to $35 an hour. This rate can swing up or down depending on the caregiver's qualifications, the complexity of the care needed, and even your zip code.

Many agencies also offer different pricing models. You might find discounted hourly rates for longer shifts, like 8-, 12-, or even 24-hour coverage, which can make a big difference in the total cost. You can dig deeper into these variables by checking out industry resources that analyze home care expenses in 2025.

This hourly figure covers a wide range of support, which can be broken down into a few main service levels. Each level comes with its own typical price range.

If there’s one thing to remember, it’s this: the "cost of home health care" isn't one single number. It’s a spectrum of prices influenced by the intensity and type of support needed, ensuring you only pay for the care that’s truly essential.

Typical Home Health Care Hourly Rates at a Glance

To give you a clearer picture of what you might pay, it helps to see how services are tiered. Different levels of care require different credentials and skills, which directly impacts the hourly rate. This table breaks down the most common service levels and what you can generally expect to pay for each.

| Service Level | Typical Hourly Rate Range | Common Services Included |

|---|---|---|

| Companion Care | $25 – $29 | Social interaction, meal prep, light housekeeping, errands, transportation. |

| Personal Care Assistance | $28 – $33 | All companion services plus hands-on help with bathing, dressing, and mobility. |

| Skilled Nursing Care | $30 – $45+ | Medical tasks like wound care, medication administration, and vital sign monitoring. |

As you can see, the rates climb as the required skill level increases. This structure ensures that you're not overpaying for basic assistance while still having access to qualified professionals when medical needs arise.

Common Service Levels and Their Costs

Let's unpack those service tiers a bit more.

-

Companion Care: This is the most basic level of support. It’s all about social interaction, helping with light housekeeping, preparing meals, and running errands. It’s perfect for someone who needs a little company and help around the house, and it typically falls on the lower end of the cost spectrum.

-

Personal Care Assistance (PCA): This next step up includes everything in companion care, plus hands-on help with what are known as Activities of Daily Living (ADLs). This means direct assistance with personal tasks like bathing, dressing, and help with mobility.

-

Skilled Nursing Care: This is the highest level of in-home care, and it must be provided by a Registered Nurse (RN) or a Licensed Practical Nurse (LPN). It involves medical tasks that require clinical training, such as wound care, administering injections or IV medications, and monitoring vital signs. Because of the expertise involved, this level of care carries the highest hourly cost.

What Drives Home Health Care Prices

If you've started looking into home health care, you've probably noticed that the prices can seem all over the map. That's because the final cost isn't a simple, one-size-fits-all number. It's a flexible total that’s built around a few critical factors, reflecting the unique needs of every family.

Think of it this way: a plane ticket from New York to Chicago costs less than one to Los Angeles. The same logic applies here—the circumstances of the care play a huge role in the final bill. Let's break down the five main things that shape the price you'll pay.

Your Geographic Location

One of the biggest drivers of cost is simple geography. The cost of living is dramatically different from state to state, and even between a major city and a quiet suburb. Those local economic realities are directly reflected in what caregivers earn.

A home health aide working in a high-cost-of-living metro area will naturally have a higher hourly rate than one in a small rural town. States with higher minimum wage laws for healthcare workers also see those costs passed on to consumers. So, care in a place like California or New York will almost certainly be more expensive than in states with lower wage floors. Your zip code is truly a foundational piece of the pricing puzzle.

The Required Level of Care

The specific type of support your loved one needs is another major piece of the equation. As we touched on before, services can range from basic companionship all the way to complex medical procedures, and the cost scales right along with the skill level required.

-

Companion Care: This is all about non-medical support—things like conversation, preparing meals, or light housekeeping. It requires the least specialized training, so it comes with the lowest hourly rate.

-

Personal Care: This level steps it up to hands-on assistance with daily activities like bathing, dressing, and help with mobility. It demands more training and physical involvement, which nudges the price up.

-

Skilled Nursing Care: When care involves medical tasks—administering medication, changing wound dressings, or managing IVs—you need a licensed nurse (an RN or LPN). This is the most expensive level of care because it relies on advanced clinical skills and credentials.

The core principle is straightforward: you pay for the expertise required. Basic companionship is less expensive than skilled medical attention because the training and qualifications of the caregiver are fundamentally different.

Caregiver Qualifications and Experience

Hand-in-hand with the level of care are the caregiver's own credentials. An aide or nurse with years of experience, special certifications in areas like dementia or palliative care, or advanced degrees will command a higher rate. It makes sense—a Certified Nursing Assistant (CNA) will cost more than a companion who doesn't have formal certifications.

Likewise, a Registered Nurse (RN) with a decade of experience in geriatric care will have a higher hourly rate than a newly licensed LPN. When you hire a caregiver, you’re investing in their knowledge, and that expertise directly impacts the quality and safety of the care your loved one receives.

The Number of Hours Needed

The sheer volume of care needed each week is another huge component of your final bill. Someone who only needs a caregiver for a few hours a week to help with errands will have a much smaller invoice than someone who requires round-the-clock supervision.

Many agencies even offer tiered pricing based on the total hours booked. A short 4-hour shift might have a higher hourly rate than a 12-hour shift or 24-hour live-in care. Why? Because longer, more consistent schedules provide more stability for the caregiver and the agency. When you're planning, think carefully about whether you need short bursts of help or continuous care, as this will dramatically change your budget.

Agency vs. Independent Provider

Finally, your choice between hiring through a home care agency or working directly with an independent caregiver will affect the price. At first glance, agencies often seem more expensive per hour, but that higher rate includes some significant, and often overlooked, benefits.

An agency handles all the administrative headaches, like payroll, taxes, and liability insurance. They also vet, train, and supervise their team, and they have a crucial backup plan if your primary caregiver gets sick. Hiring an independent caregiver might look cheaper upfront, but you instantly become the employer, making you responsible for all those legal and logistical details yourself.

How Home Care Costs Compare to Other Options

When you start looking into home health care, it's easy to get sticker shock. But you can't look at the cost in a vacuum. To really understand the value, you have to stack it up against the other major senior care options.

For most families, this isn't just about finding any care; it's about finding the right care at a price that doesn't break the bank. When you lay the numbers out side-by-side, you often find that keeping a loved one at home is one of the smartest financial moves you can make.

Think of it like you're shopping for a car. You wouldn't just look at the price of one model without comparing it to others in its class. In the same way, looking at the costs of assisted living and nursing homes gives you the full picture, showing where home health care truly shines.

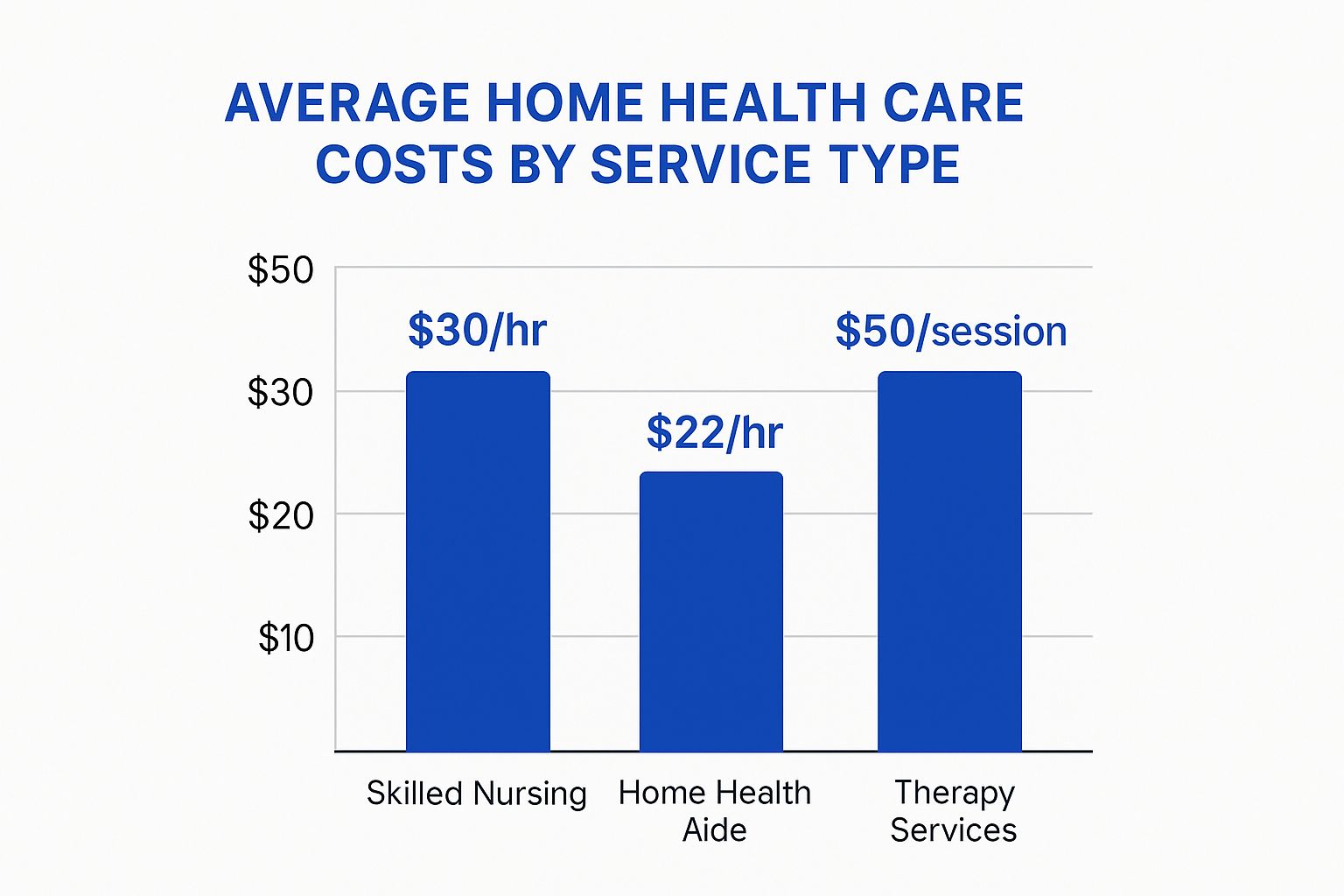

This graphic gives a great snapshot of the typical hourly costs for different home health services.

As you can see, the price lines up directly with the level of medical skill needed. This lets you build a care plan that’s customized to your needs and, quite often, much more affordable.

The Financial Case for Aging in Place

Most seniors want to stay in their own homes because it’s comfortable and familiar, but there’s a powerful financial argument for it, too. As long as care needs are moderate, home health care almost always comes out as the more budget-friendly option compared to a residential facility.

Why? Because you’re only paying for the specific hours of care you actually need. You’re not footing the bill for the 24/7 overhead that comes with running an entire facility.

This flexibility is a huge deal. If your mom only needs a hand for a few hours each morning, that's all you pay for. Assisted living or nursing homes, on the other hand, charge a flat monthly fee that covers everything from room and board to activities you might never use. Home care costs can be tailored to fit your exact situation, so you aren't paying for a bunch of extras you don't need.

Sure, the cost of home care has been creeping up due to higher caregiver wages and inflation. But even so, it frequently remains the most economical choice. For example, in Massachusetts, the annual cost for full-time home care was about $86,944 in 2024. In that same state, a semi-private room in a nursing home ran around $173,375 a year—literally double the price. You can get more details on these home health care industry trends and how they might affect your budget.

Comparing Assisted Living and Nursing Homes

To feel confident in your decision, you have to understand what you're getting with the alternatives. Both assisted living communities and nursing homes offer different levels of care at very different price points.

-

Assisted Living Facilities: These are communities built for people who need a bit of help with daily tasks but don't require round-the-clock medical attention. The monthly fee usually covers an apartment, meals, and social events, but you'll often pay extra for personal care services.

-

Nursing Homes: This is the highest level of care available outside of a hospital. It includes 24/7 medical supervision and skilled nursing services. As you might expect, it's also the most expensive option, with costs that can easily top $100,000 a year.

The bottom line is this: while facility-based care offers an all-in-one package, that all-inclusive price can be a massive financial burden, especially when all your loved one really needs is a few hours of support each day.

A Head-to-Head Cost Comparison

Let’s get down to the numbers. The national averages below are a great starting point, but just remember that the actual costs in your area will depend on your location and the exact services you need.

Annual Senior Care Cost Comparison

Here’s a simple breakdown of the average annual costs for the three main types of senior care, giving you a clear, side-by-side view.

| Type of Care | Average Annual National Cost | Key Benefits |

|---|---|---|

| Home Health Care | ~$61,776 (44 hrs/week) | Personalized one-on-one care in a familiar environment; flexible scheduling. |

| Assisted Living Facility | ~$64,200 | Community setting with social activities; includes housing and meals. |

| Nursing Home | ~$108,405 (Semi-Private Room) | 24/7 skilled medical care and supervision for complex health needs. |

This table really drives home a critical point: for anyone who doesn't need constant medical oversight, home health care delivers a powerful mix of personalized attention and financial common sense. It allows families to put their money toward the specific support that will make the biggest difference, all while honoring their loved one's wish to stay right where they belong—at home.

Your Guide to Paying for Home Health Care

Once you understand the numbers behind the cost of home health care, the next big question is a practical one: how do we actually pay for it? For many families, figuring out the funding can feel like staring at a complex puzzle with half the pieces missing.

The good news is that you're not on your own. There are several well-established paths to make care affordable and accessible. Think of this guide as your map through that maze. We’ll walk through the primary funding sources one by one, so you can build a solid financial strategy for your loved one's care with confidence, not confusion.

Exploring Private Pay Options

The most straightforward way to cover home health care is through private pay. This simply means using personal funds—like savings, pension income, or investments—to pay for services directly.

This approach gives you the most freedom and control. There are no eligibility hoops to jump through or outside restrictions on the type or amount of care you can arrange. Whether you need a few hours of companionship a week or 24/7 skilled nursing support, you can hire the exact caregiver or agency that fits your needs.

Using Long-Term Care Insurance

For those who planned ahead with a long-term care (LTC) insurance policy, this can be an incredibly powerful tool. These policies are specifically designed to cover care services that regular health insurance often won't, including the hands-on, in-home help with daily activities.

To start using your LTC policy, you’ll first need to activate your benefits. This typically involves getting a note from a healthcare professional certifying that you need help with a certain number of Activities of Daily Living (ADLs), like bathing or dressing.

It's crucial to pull out your policy and review the fine print. Pay close attention to:

- The daily or monthly benefit amount: This is the maximum your policy will pay out.

- The elimination period: Think of this as a deductible—it's a waiting period you have to cover out-of-pocket before benefits kick in.

- Covered services: Most policies are comprehensive, but it never hurts to confirm exactly what's included.

Understanding Medicare Coverage for Home Health

This is a big one, because it’s a common point of confusion. Many families assume Medicare will cover long-term home care, but its role is actually quite limited and specific. Medicare is built for short-term, skilled medical care after an event like an illness, injury, or hospital stay. It was never intended for ongoing custodial care (non-medical help with daily life).

Medicare will cover home health services only if they are deemed medically necessary, ordered by a doctor, and involve intermittent skilled nursing care or therapy. It will not pay for 24-hour care or personal care aides if that is the only help you need.

The distinction is critical. If your mom needs help with cooking and getting around the house, Medicare won't step in. But if she needs a registered nurse to change a surgical dressing, it likely will—for a limited time.

Tapping into Medicaid Benefits

For individuals with limited income and assets, Medicaid is a vital lifeline. Unlike Medicare, Medicaid does cover long-term custodial care at home. The eligibility rules are strict and vary from state to state, but for those who qualify, it can be the key to making sustained home care a reality.

Many states have Home and Community-Based Services (HCBS) waivers. These are fantastic programs that allow people who would otherwise qualify for a nursing home to receive comprehensive care services right in their own homes. These waivers can cover everything from personal care aides and skilled nursing to home modifications and meal deliveries, all with the goal of keeping people in the community.

Accessing VA Benefits for Veterans

Veterans enrolled in the VA healthcare system may be eligible for several programs that help pay for home care. The standard VA health benefits package can include services like skilled nursing, physical therapy, and help with daily activities.

One of the most valuable resources is the Aid and Attendance benefit. This is an increased monthly pension payment available to qualified veterans and their surviving spouses. The funds are flexible and can be used to purchase home care services to assist with daily living. To qualify, veterans must meet certain service, income, and disability criteria. It’s a well-earned benefit for those who have served our country.

How New Care Models Are Changing Costs

The old way of paying for healthcare often feels like you're playing defense. A health crisis strikes, you rush to the hospital, and a massive bill isn't far behind. But the home health world is flipping the script, moving toward smarter, more proactive approaches that aim to prevent those expensive emergencies in the first place.

These newer models are all about delivering better health outcomes, not just billing for more services. Think of it like this: you can either pay for regular, affordable oil changes to keep your car's engine running smoothly, or you can wait for a major breakdown that costs a fortune to fix. Proactive care is the oil change—it keeps things in check to avoid bigger, more expensive problems down the road.

This shift is more than just a passing trend. It’s a fundamental change in how we think about and pay for care, and it can lead to serious savings for families while giving their loved ones a better quality of life.

The Rise of Value-Based Care

One of the biggest game-changers is the move to value-based care. In this model, home health agencies get paid based on the quality of their care, not the sheer quantity of visits. Instead of simply billing for every task, providers are financially motivated to keep patients healthy and, most importantly, out of the hospital.

For your family, this means the care team is genuinely invested in preventing setbacks. They're laser-focused on things like:

- Medication Management: Making absolutely sure prescriptions are taken correctly to avoid dangerous mix-ups or side effects.

- Fall Prevention Programs: Putting strategies in place to lower the risk of injuries that often lead to hospital stays.

- Chronic Disease Management: Actively monitoring conditions like diabetes or heart disease to keep them stable and under control.

This focus on prevention has a direct impact on your wallet. Every time a home health agency successfully prevents a hospital readmission, it saves everyone—the healthcare system and often your family—thousands of dollars.

Hospital at Home: A Game-Changing Model

An even more direct cost-saving innovation is the Hospital-at-Home (HaH) model. This approach does exactly what it sounds like: it brings hospital-level care right into a person's home, offering a safe and effective alternative to a traditional inpatient stay for many conditions.

The Hospital-at-Home model isn't just about comfort; it's a proven strategy for reducing costs while delivering high-quality medical treatment. By leveraging technology and skilled professionals, it turns a patient's home into their recovery room.

This model is catching on fast. The U.S. home health care sector is on track to hit a valuation of $107.07 billion by 2025, and programs like HaH are a major reason why. Already, more than 350 hospitals across 37 states have rolled out HaH programs, providing top-tier treatment where patients feel most at ease.

The numbers speak for themselves: the average HaH admission costs around $5,800, a significant drop from the $7,700 price tag for a typical hospital stay. You can dig deeper into these U.S. home care industry stats to see the bigger picture.

By cutting out the massive overhead costs of a hospital facility, the HaH model creates immediate and substantial savings. It's a powerful tool for managing the cost of acute medical care without compromising on quality. Knowing about these emerging options can help you make smarter, more cost-effective decisions for your family's care, both now and in the years to come.

Answering Your Top Home Care Cost Questions

As you dive into the financial side of home health care, it’s completely normal for specific, practical questions to pop up. Once you get past the basics of what drives costs and how to pay for care, you're often left with a few "what ifs" that need clearing up.

This section is your go-to Q&A. We've pulled together the most common questions we hear from families as they put the finishing touches on their care plans. Each answer is designed to give you not just a quick response, but the context you need to move forward with real confidence.

Does Medicare Cover 24/7 In-Home Care?

This is easily one of the most frequent questions we get, and the short answer is no. Medicare's home health benefit is really designed for short-term, medically necessary care after an illness, injury, or hospital stay. It was never intended to cover long-term, round-the-clock custodial care.

Medicare will only step in to cover home health services if a doctor certifies that you need intermittent skilled nursing or therapy. It won't pay for personal care aides who help with daily living if that’s the only support needed. For families who need 24/7 supervision, you’ll need to look at other funding sources like long-term care insurance, Medicaid, or private pay.

Are Any Home Health Care Expenses Tax-Deductible?

Yes, they absolutely can be, and this can provide some significant financial relief for families. If you, your spouse, or a dependent are receiving care for a chronic illness, the costs for medical services are often deductible. This can include payments for nursing and other types of care prescribed by a physician.

The key is that the expenses must be for medical care—meaning the services are mainly for diagnosing, treating, or preventing a physical or mental illness.

Here’s a quick look at what usually qualifies:

- Skilled nursing services from an RN or LPN.

- Therapy services, such as physical, occupational, or speech therapy.

- Personal care services, but only if they are necessary for a chronically ill person to manage their daily activities.

The most important piece of the puzzle is that the care plan must be prescribed by a licensed health care practitioner. It's always smart to chat with a qualified tax advisor to see how these deductions apply to your specific situation and make sure you're meeting all the IRS rules.

How Can I Find Affordable Care In My Area?

Finding high-quality care that doesn't break the bank takes a little bit of research. The real goal isn’t just to find the "cheapest" option, but to find the best value—excellent support for your loved one without completely straining your budget.

A fantastic place to start is your local Area Agency on Aging (AAA). These are non-profit organizations designated by the state to help older adults and their families. They can connect you with a treasure trove of local resources, including vetted home care agencies and information on financial aid programs. They're an invaluable, unbiased source of help.

Beyond that, don't be shy about interviewing multiple home care agencies.

- Get detailed pricing sheets from at least three different providers to compare.

- Ask about different service levels or if they offer better rates for longer shifts.

- Inquire about how they screen and train their caregivers.

Doing this homework will give you a solid feel for the local market rate and help you pinpoint the agency that’s the best fit for your family.

Can I Use a Reverse Mortgage to Pay for Care?

For some homeowners aged 62 or older, a reverse mortgage can be a practical financial tool. It essentially lets you convert a piece of your home's equity into cash, which you can then use for home health care expenses. The loan is usually paid back when the homeowner sells the house, moves out permanently, or passes away.

This can be a great way to access funds for care while staying in the comfort of your own home. But it's a major financial decision with lasting consequences.

Before you even consider a reverse mortgage, it is critical to speak with a federally approved reverse mortgage counselor. They provide impartial advice and will make sure you understand all the benefits, risks, and obligations that come with this type of loan.

What Happens if My Caregiver Is Sick or on Vacation?

This is a crucial question that gets right to the heart of one of the biggest differences between hiring through an agency versus hiring someone privately. If you hire an independent caregiver, you are the employer. That means if your aide is sick or wants a vacation, it’s on you to find a replacement.

A reputable home care agency, on the other hand, has a plan for this. They maintain a team of qualified caregivers and will arrange for a substitute to step in, ensuring there are no gaps in care. This provides incredible peace of mind for families, who know their loved one will always have the support they need. When you’re talking to agencies, always ask them to walk you through their backup care procedures.

At NJ Caregiving, we know that finding the right care solution brings up a lot of questions. Our team is here to offer clear answers and compassionate support to families in Princeton, NJ, and throughout Mercer County. If you need personalized guidance on building an effective and affordable care plan, we're here to help. Discover how our skilled caregivers can enhance your loved one's independence and quality of life by visiting us at https://njcaregiving.com.